UK Junior ISA (JISA) Statistics 2026

Key UK Junior ISA Statistics 2026

- £1.8 billion was subscribed into Junior ISAs during 2023/24 across 1.37 million accounts — a 20% increase on the prior year and the highest annual JISA subscription on record.

- £1.15 billion went into Stocks & Shares JISAs in 2023/24 — the first time investment subscriptions surpassed £1 billion, representing 63.6% of all JISA money.

- £9 billion+ total JISA holdings — split ~£5bn in S&S JISAs and ~£4bn in Cash JISAs. A 77-fold increase from £117m at launch in 2011.

- 758,000 matured Child Trust Fund accounts worth £1.5 billion remain unclaimed as of April 2025 — with 27,000 accounts holding £10,000 or more.

- 14–15% of eligible children had an active Junior ISA in 2023/24 — leaving the majority of UK children without any tax-free savings.

- £1,347 per year average JISA subscription — just 15% of the £9,000 allowance. The average S&S JISA subscriber (£1,807) contributes more than double the average Cash JISA subscriber (£856).

- £20,802 vs £7,453 — £9,000 in a global equity fund over 18 years vs a Cash JISA in real terms, an almost 3× gap.

- Doubled in 2020 — the JISA allowance was more than doubled from £4,368 to £9,000 in the March 2020 Budget and has been frozen since, confirmed frozen until at least April 2031.

- +52% Fidelity reported a 52% increase in JISA openings in January–October 2025 vs 2024, driven by IHT planning and cost-of-living pressures.

- January 2029 — the first JISAs opened at birth will mature, as children born on 3 January 2011 turn 18.

2023/24

Market Value

Subscribed 2023/24

(April 2025)

How Many Junior ISAs Are There in the UK?

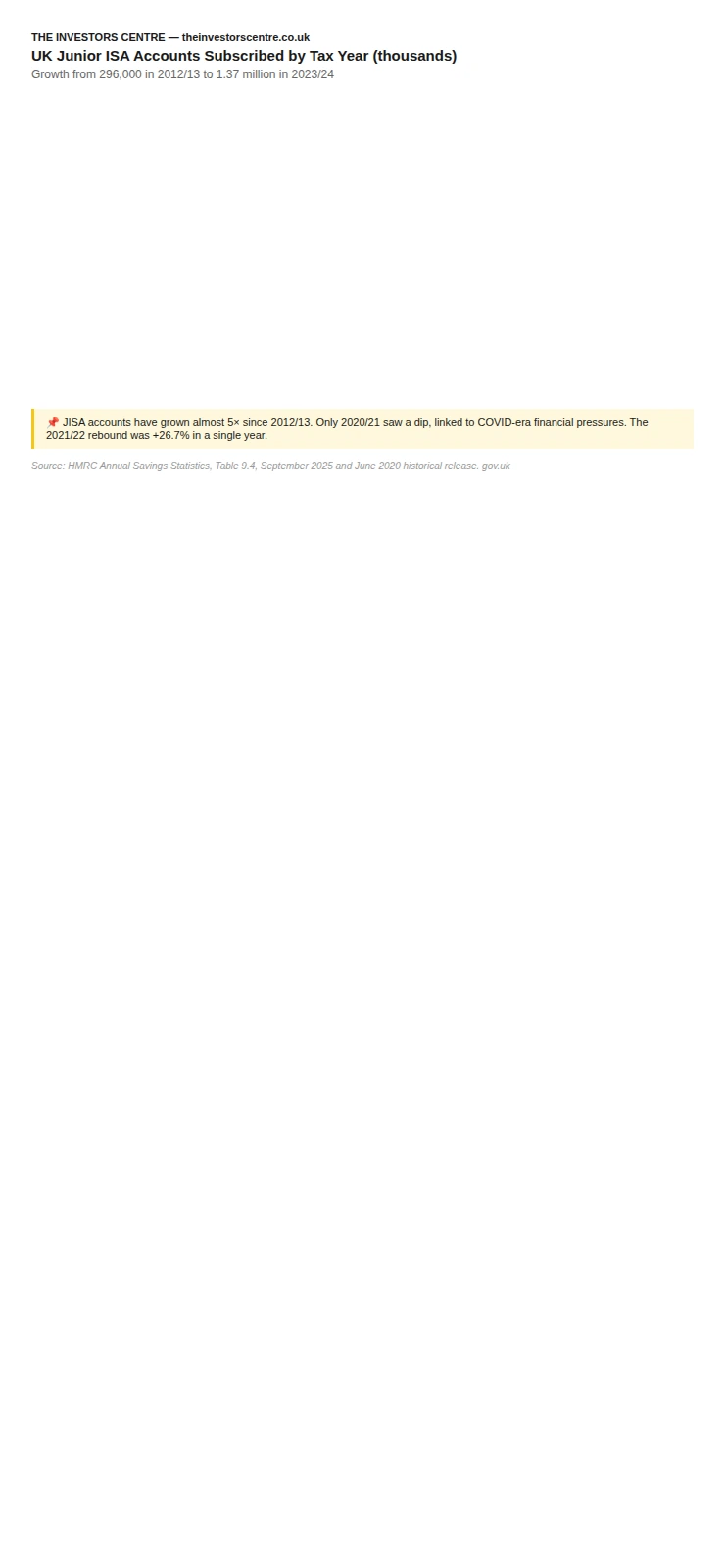

1.37 million Junior ISA accounts received contributions in 2023/24 — a 9.6% increase on the prior year. The number of actively subscribed JISAs has grown from just 296,000 in 2012/13 to a record high in 2023/24, representing sustained growth across every year except a brief COVID-related dip in 2020/21.

Only around 14–15% of JISA-eligible children had an active account in 2023/24. This low penetration rate reflects a combination of awareness gaps — 82% of cash savers know S&S JISAs exist but only 25% know anything about them (Investment Association, 2025) — and affordability pressures on families.

Source: HMRC Annual Savings Statistics, Table 9.4 (September 2025 and June 2020 historical release).

| Tax Year | Total Accounts (000s) | Cash JISA | S&S JISA | YoY Change |

|---|---|---|---|---|

| 2012/13 | 296 | 204 | 92 | — |

| 2014/15 | 510 | 365 | 145 | +18.1% |

| 2016/17 | 794 | 569 | 225 | +7.6% |

| 2018/19 | 954 | 668 | 286 | +5.2% |

| 2021/22 | ~1,210 | — | — | +26.7% |

| 2022/23 | ~1,250 | — | — | +3.3% |

| 2023/24 | ~1,370 | — | — | +9.6% |

Source: HMRC Annual Savings Statistics, Table 9.4.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

Junior ISA Subscriptions: The Shift from Cash to Investment

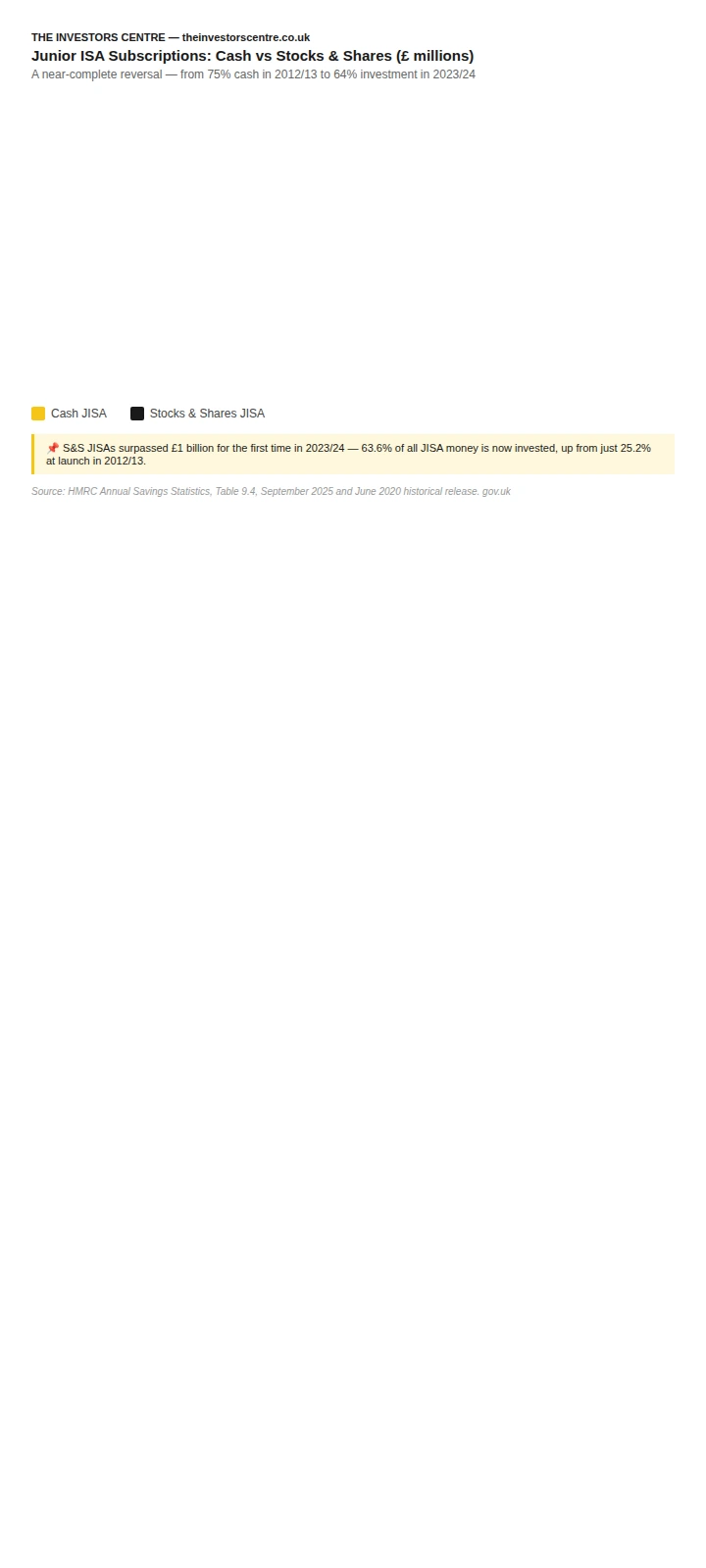

£1.8 billion was subscribed into JISAs in 2023/24 — a 20% increase on 2022/23. The most significant structural change in the JISA market is the sustained shift from Cash JISAs to Stocks & Shares JISAs. In 2012/13, cash accounted for 74.8% of JISA subscriptions. By 2023/24, investments accounted for 63.6% — a near-complete reversal over 11 years.

This shift reflects both a generational change in attitudes toward investing and the lower opportunity cost of investing — with a very long time horizon of up to 18 years, even conservative parents are increasingly recognising that equity investment outperforms cash over such periods. Parents shopping for a provider can compare platforms that offer a Stocks and Shares JISA alongside adult ISAs.

| Tax Year | Cash (£m) | S&S (£m) | Total (£m) | Cash % | S&S % |

|---|---|---|---|---|---|

| 2012/13 | 294 | 99 | 393 | 74.8% | 25.2% |

| 2015/16 | 522 | 399 | 921 | 56.7% | 43.3% |

| 2018/19 | 555 | 419 | 974 | 57.0% | 43.0% |

| 2022/23 | ~633 | ~867 | 1,500 | 42.2% | 57.8% |

| 2023/24 | ~655 | ~1,145 | 1,800 | 36.4% | 63.6% |

Source: HMRC Annual Savings Statistics, Table 9.4.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

"A 75/25 cash-to-investment split flipping to 36/64 over 11 years is one of the most striking behavioural shifts in UK retail saving. Parents are doing what individual investors have been slow to do in adult ISAs — recognising that an 18-year horizon is almost definitionally a horizon where equities dominate cash. If we see the same logic applied when the 2029 wave of matured JISAs rolls into adult ISAs, the UK retail investing base is about to expand meaningfully."

— Adam Woodhead, Senior Analyst, The Investors Centre

Total Junior ISA Market Value: £9 Billion and Growing

Total JISA holdings have grown from £117 million at inception to over £9 billion — a 77-fold increase in 12 years. Approximately £5 billion is held in Stocks & Shares JISAs and £4 billion in Cash JISAs, reflecting the gradual shift towards investment across the market. The average JISA subscription of £1,347 per year represents just 15% of the £9,000 allowance, meaning most JISA balances at age 18 will be far below the maximum possible.

| Year End | S&S Value (£m) | Cash Value (£m) | Total (£m) | Growth from Prior |

|---|---|---|---|---|

| April 2013 | 167 | 390 | 557 | — |

| April 2015 | 515 | 1,140 | 1,655 | +197% |

| April 2017 | 1,370 | 1,969 | 3,339 | +102% |

| April 2019 | 2,280 | 2,588 | 4,868 | +46% |

| April 2024 (est.) | ~5,000 | ~4,000 | ~9,000 | (+84% on 2019) |

Source: HMRC Annual Savings Statistics, Table 9.6 (June 2020 historical release); April 2024 estimate from AJ Bell analysis, September 2025.

Child Trust Funds: 758,000 Unclaimed Accounts Worth £1.5 Billion

The Child Trust Fund was introduced by the Labour government in 2002 and ran until January 2011, providing every eligible child with a government seed payment of £250 (£500 for lower-income families). Approximately 6.3 million accounts were opened. The first CTFs matured in September 2020, when children born in September 2002 turned 18.

As of April 2025, 758,000 matured CTF accounts remain unclaimed, holding a total of £1.5 billion. Of these, 27,000 accounts hold £10,000 or more. The unclaimed rate has improved from 45% in 2021 to 25% in 2025, but the absolute number of unclaimed pots continues to rise as more accounts mature each year.

HMRC offers a free CTF finder at gov.uk/child-trust-funds. The Share Foundation also operates a simplified finder at findctf.sharefound.org. HMRC warns against commercial third-party finders, some of which charge up to £350 or 25% of account value — a reminder to use the free resources on HMRC and our TIC investing library before trusting third-party "finders."

| Metric | April 2022 | April 2024 | April 2025 |

|---|---|---|---|

| Matured CTFs (total) | ~956,000 | ~2,333,000 | ~3,043,000 |

| Claimed or transferred | ~528,000 | ~1,662,000 | ~2,285,000 |

| Unclaimed matured accounts | ~428,000 | ~671,000 | 758,000 |

| Unclaimed rate | ~45% | ~29% | ~25% |

| Total remaining CTF value | — | — | £7.5 billion |

Source: HMRC CTF Tables, September 2025; HMRC press release; AJ Bell analysis.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

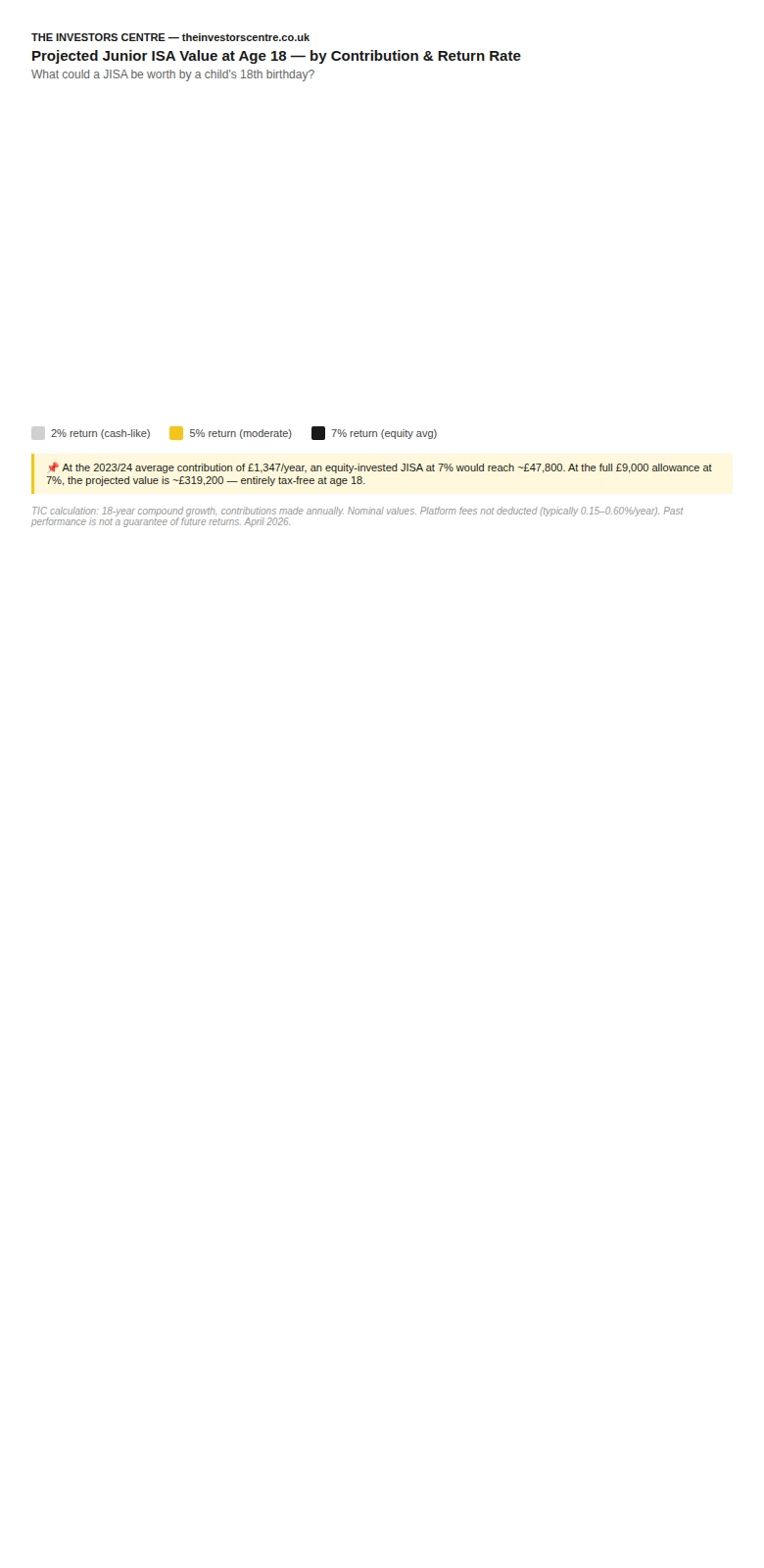

TIC Analysis: What Could a JISA Be Worth at Age 18?

The table below shows projected JISA values at age 18 for different annual contribution levels and return scenarios. The £1,347 average contribution row reflects actual 2023/24 HMRC data. The maximum £9,000 row shows the full potential of the allowance. Over an 18-year horizon, platform fee drag compounds materially — so the choice of UK investment platforms matters more here than in almost any other wrapper.

| Annual Contribution | Return: 2% (cash-like) | Return: 5% (moderate) | Return: 7% (equity avg) | Return: 9% (high growth) |

|---|---|---|---|---|

| £600/yr (£50/month) | ~£13,200 | ~£17,500 | ~£21,300 | ~£26,200 |

| £1,347/yr (2023/24 avg) | ~£29,600 | ~£39,200 | ~£47,800 | ~£58,800 |

| £3,000/yr (£250/month) | ~£65,800 | ~£87,200 | ~£106,400 | ~£130,800 |

| £9,000/yr (full allowance) | ~£197,400 | ~£261,600 | ~£319,200 | ~£392,300 |

TIC calculation, April 2026.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

"Even at the UK-average contribution of £1,347 a year, an equity-invested JISA at 7% reaches roughly £47,800 by age 18 — not transformational by itself, but a deposit contribution that closes most regional first-home gaps outside London. The real lesson of the model is that the first 5% of fee drag does more damage than the last 2% of return volatility. Pick the wrapper carefully; pick the provider even more carefully."

— Adam Woodhead, Senior Analyst, The Investors Centre

Junior ISA Allowance History: From £3,600 to £9,000

The Junior ISA launched on 1 November 2011 with an annual allowance of £3,600. It was increased incrementally via CPI indexation each year until the March 2020 Budget, when Chancellor Rishi Sunak more than doubled it from £4,368 to £9,000 in a single announcement. The allowance has been frozen at £9,000 since April 2020 and is confirmed frozen until at least April 2031.

Real-terms erosion: The £9,000 allowance set in April 2020 is worth approximately £7,350 in real terms at April 2026 prices, having lost around 18% of its purchasing power to inflation. To maintain its real value, the allowance would need to be approximately £10,700 in 2026/27.

| Tax Year | JISA Annual Allowance | Key Event |

|---|---|---|

| 2011/12 | £3,600 | JISA launched 1 November 2011 |

| 2013/14 | £3,720 | Annual CPI indexation begins |

| 2014/15 | £4,000 | Increased from 1 July 2014 (Budget 2014) |

| 2017/18 | £4,128 | CPI-linked increase |

| 2019/20 | £4,368 | Final pre-doubling figure |

| 2020/21 | £9,000 | More than doubled in Budget 2020 (6 April 2020) |

| 2025/26 | £9,000 | Frozen; confirmed frozen until April 2031 |

Source: HMRC; HM Treasury; GOV.UK Tax-free savings newsletter 19, November 2025.

Frequently Asked Questions

What is a Junior ISA?

A Junior ISA (JISA) is a tax-free savings account for children under 18 who are UK residents. Interest, capital gains, and dividends earned within a JISA are completely free of UK tax. The annual allowance is £9,000 for 2025/26. Money is locked until the child's 18th birthday. Anyone can contribute, but only a parent or guardian can open the account. Source: GOV.UK.

How many Junior ISAs are there in the UK?

1.37 million Junior ISA accounts were actively subscribed to in 2023/24 — a record high. The total number of open JISA accounts (including dormant ones) is not published by HMRC, but the total market value of approximately £9 billion across an estimated 2+ million accounts suggests this is considerably higher. Source: HMRC Annual Savings Statistics, September 2025.

How much is in Junior ISAs in the UK?

Total JISA holdings are estimated at over £9 billion — approximately £5 billion in Stocks and Shares JISAs and £4 billion in Cash JISAs. This represents a 77-fold increase from £117 million at the product's launch in 2011. Source: AJ Bell analysis of HMRC data, September 2025.

What is the Junior ISA allowance for 2025/26?

The Junior ISA annual allowance is £9,000 for 2025/26. A child can hold one Cash JISA and one Stocks and Shares JISA simultaneously, but combined contributions must not exceed £9,000 per tax year. The allowance is separate from the adult ISA allowance of £20,000. Source: HM Treasury; GOV.UK.

What is the difference between a Cash JISA and a Stocks and Shares JISA?

A Cash JISA pays a fixed or variable interest rate, like a savings account. The best rate available in April 2026 is 3.85% AER. A Stocks and Shares JISA invests in funds, shares, or bonds, with the potential for higher long-term returns but with investment risk. Over 18 years, equity investments have historically significantly outperformed cash. Source: Which?, April 2026.

What is the best Junior ISA rate in 2026?

The best Cash JISA rate in April 2026 is 3.85% AER (Leek Building Society), followed by Skipton Building Society at 3.80% AER and Coventry Building Society at 3.75% AER. NS&I offers 3.55% AER with a 100% government guarantee. For Stocks and Shares JISAs, Hargreaves Lansdown, InvestEngine (0% fee), and Vanguard (0.15%/year) are consistently top-rated. Source: Which?; MoneySavingExpert, April 2026.

What percentage of children have a Junior ISA?

Approximately 14–15% of JISA-eligible children had an active Junior ISA in 2023/24. This low uptake rate reflects awareness gaps and affordability pressures. The Investment Association found that 82% of cash savers know Stocks and Shares JISAs exist, but only 25% know anything about them. Source: TIC calculation; Investment Association, April 2025.

What happens to a Junior ISA when the child turns 18?

At age 18, the JISA automatically converts to an adult ISA. The parent or guardian loses access, and the 18-year-old becomes the sole account holder with full control. The matured JISA balance does not count against the adult's £20,000 ISA allowance — it sits above it as an additional tax-free sum. Source: GOV.UK.

When will the first Junior ISAs mature?

The first JISAs opened for children born from birth (3 January 2011) will mature in January 2029. However, some JISAs opened for older children without Child Trust Funds matured earlier. The years 2029–2031 will see the largest wave of JISA maturities as the first generation of birth-to-18 JISA savers reaches adulthood. Source: GOV.UK.

Can I access a Junior ISA early?

No — Junior ISA funds are locked until the child's 18th birthday. Early withdrawals are only permitted in two circumstances: terminal illness of the child (subject to HMRC approval) or the death of the child. There is no court order provision for early access. Source: GOV.UK.

What is a Child Trust Fund and can I still get one?

A Child Trust Fund (CTF) was a government savings scheme for children born between 1 September 2002 and 2 January 2011. It was replaced by the Junior ISA in 2011 and is now closed to new applicants. Approximately 6.3 million CTF accounts were opened. As of April 2025, 758,000 matured CTF accounts worth £1.5 billion remain unclaimed. Source: HMRC CTF Tables, September 2025.

How do I find a lost Child Trust Fund?

HMRC offers a free online CTF finder at gov.uk/child-trust-funds, accessible via Government Gateway. The Share Foundation operates a simplified finder at findctf.sharefound.org for those without Government Gateway access. You can also write to HMRC directly. HMRC warns against using commercial third-party CTF finder services, some of which charge fees of up to £350 or 25% of the account value.

Can I transfer a Child Trust Fund to a Junior ISA?

Yes — since April 2015, CTF holders can transfer to a Junior ISA. The full CTF balance must be transferred (partial transfers are not permitted), and the child cannot hold both simultaneously. The transferred amount does not count toward the £9,000 annual JISA allowance. Source: HMRC; TISA.

Can grandparents open or contribute to a Junior ISA?

Grandparents (and any other person) can contribute to an existing Junior ISA, but only a parent or guardian with parental responsibility can open a new JISA on the child's behalf. A child aged 16 or 17 can open their own JISA. There is no limit on the number of contributors, only on the total annual subscription (£9,000). Source: GOV.UK; HMRC.

How much could a Junior ISA be worth at age 18?

At the 2023/24 average contribution of £1,347 per year, invested in equities at 7% annual growth, a JISA would reach approximately £47,800 by age 18. At the full £9,000 annual allowance at 7% growth, the projected value is approximately £319,200. Even modest savings of £50 per month at 5% growth would reach approximately £17,500. Source: TIC calculation, April 2026.