- expertise:

- Platform Testing, Cryptocurrency, Retail Investing

- credentials:

- Active investor since 2013 · 11+ years experience

- tested:

- 50+ platforms · 200+ guides authored

- expertise:

- CFD Trading, Forex, Derivatives, Risk Management

- credentials:

- Chartered ACII (2018) · Trading since 2012

- tested:

- 40+ forex & CFD platforms with live accounts

How We Test

Real accounts. Real money. Real trades. No demo accounts or press releases.

What we measure:

- Spreads vs advertised rates

- Execution speed and slippage

- Hidden fees (overnight, withdrawal, conversion)

- Actual withdrawal times

Scoring:

Fees (25%) · Platform (20%) · Assets (15%) · Mobile (15%) · Tools (10%) · Support (10%) · Regulation (5%)

Regulatory checks:

FCA Register verification · FSCS protection

Testing team:

Adam Woodhead (investing since 2013), Thomas Drury (Chartered ACII, 2018), Dom Farnell (investing since 2013) — 50+ platforms with funded accounts

Quarterly reviews · Corrections: in**@*******************co.uk

Disclaimer

Not financial advice. Educational content only. We're not FCA authorised. Consult a qualified advisor before investing.

Capital at risk. Investments can fall. Past performance doesn't guarantee future results.

CFD warning. 67-84% of retail accounts lose money trading CFDs. High risk due to leverage.

Contact: in**@*******************co.uk

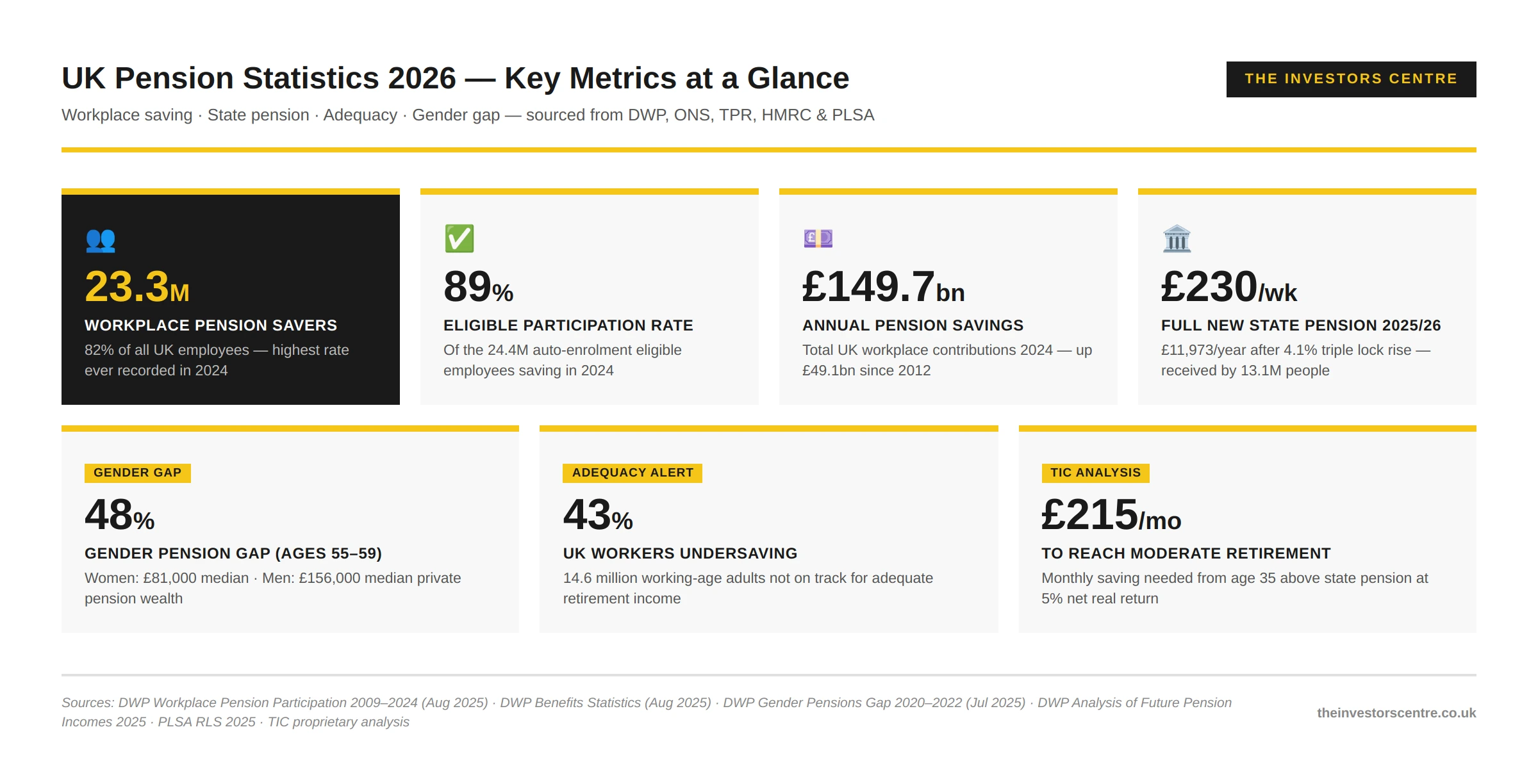

Key UK Pension Statistics 2026

- 23.3 million UK employees were actively saving into a workplace pension in 2024 — representing 82% of all employees.

- 89% of eligible employees (those meeting auto-enrolment criteria) were saving into a workplace pension in 2024 — the highest rate ever recorded.

- £149.7 billion in total annual workplace pension savings in 2024 — a real-terms increase of £49.1 billion since auto-enrolment began in 2012.

- 13.1 million UK adults received the state pension in February 2025, receiving a mean of £202.62 per week.

- £230.25 per week (£11,973/year) — the full new state pension rate for 2025/26 following a 4.1% triple lock increase.

- 43% (14.6 million) of working-age people in the UK are undersaving for retirement against their Target Replacement Rate — up from 38%.

- 48% gender pension gap among UK adults aged 55–59 — women hold median private pension wealth of £81,000 vs £156,000 for men.

- 74% of UK private sector defined benefit pension schemes are now closed to future accrual — just 160 remain fully open.

- 3.3 million pension pots are estimated to be lost in the UK, containing a combined £31.1 billion in unclaimed savings.

- £55.4 billion — the estimated total annual cost of pension tax relief (income tax + NICs) to the UK Government in 2024/25.

- 20% of self-employed UK adults pay into a pension — a dramatic fall from 50% in the late 1990s, and one of the most critical gaps in UK retirement saving.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

How Many People Have a Pension in the UK?

In 2024, 23.3 million employees in the UK were actively saving into a workplace pension — 82% of the total employed workforce. Among the 24.4 million employees who meet auto-enrolment eligibility criteria (aged 22–state pension age, earning above £10,000), the participation rate was 89%.

The total number of individuals with any form of private pension (workplace or personal) is significantly higher. The ONS Wealth and Assets Survey (Wave 7, 2018–2020) found that 78% of adults of working age and above held some private pension wealth.

| Year | Employees Saving (m) | % All Employees | % Eligible Employees |

|---|---|---|---|

| 2012 (pre-AE) | 9.2 | 54% | 55% |

| 2015 | 14.1 | 63% | 70% |

| 2018 | 18.8 | 73% | 84% |

| 2020 | 19.2 | 74% | 86% |

| 2022 | 22.6 | 79% | 88% |

| 2023 | 22.6 | 79% | 88% |

| 2024 | 23.3 | 82% | 89% |

Source: DWP Workplace Pension Participation and Savings Trends 2009–2024, August 2025.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

Auto-Enrolment Has Added 11.4 Million Pension Savers Since 2012

Auto-enrolment, introduced in October 2012, is the single most transformative change to UK pension saving in a generation. By February 2026, a cumulative 11,416,000 eligible jobholders had been automatically enrolled into a qualifying pension scheme — workers who might otherwise have saved nothing.

A further 12,394,000 workers were already active members of a qualifying scheme at their employer's staging date, meaning the policy has reinforced existing saving as well as generating new savers. A total of 2,693,697 employers have now completed their declaration of compliance with TPR.

Who Is Still Being Left Behind by Auto-Enrolment?

- Micro employers (fewer than 5 employees): Only 59% of eligible employees save — a 30-percentage-point gap below the national average.

- Self-employed: Just 20% pay into any pension — down from 50% in the late 1990s. Auto-enrolment does not apply to the self-employed.

- Pakistani and Bangladeshi workers: 68% participation rate (3-year average) — 21ppt below the national average.

- Non-eligible employees (earning below £10,000): Only 33% were saving in 2024, up from 28% the previous year.

"Auto-enrolment has solved the participation problem but not the adequacy problem. Getting 89% of eligible employees saving was the easy leg — raising the minimum contribution from 8% of qualifying earnings to something approaching a realistic replacement rate is the one that actually determines whether the next 40 years of retirements are comfortable. Every year without a contribution-rate review is a year millions of workers fall further behind their own future."

The Shift from Defined Benefit to Defined Contribution Pensions

The UK workplace pension landscape has undergone a structural transformation over the past three decades. Defined benefit (DB) schemes — which guarantee a specific income in retirement — have been steadily closed in favour of defined contribution (DC) schemes, where retirement income depends on investment performance.

The consolidation of the DC market is striking: the number of non-micro DC trust-based schemes fell 15% in a single year to under 1,000 for the first time in 2024, then to 790 in 2025. Meanwhile, 33 master trusts now hold 92% of all DC trust-based memberships — 30.1 million of 32.8 million total DC members. DB scheme funding has dramatically improved: 82% of private sector DB schemes are now in surplus as at 2025, with an aggregate funding level of 118% against technical provisions — a surplus of £167 billion.

| Scheme Type | Schemes | Membership | Assets | Status |

|---|---|---|---|---|

| Private sector DB/hybrid | 5,060 | 9.17m | £1,102bn | 74% closed to future accrual |

| Public sector DB | ~200 | 19.78m | £548bn | Largely open |

| DC trust-based (non-micro) | ~790 | 32.8m (2025) | £249bn | Growing via master trusts |

| DC micro (2–11 members) | ~24,680 | Small | Minimal | Declining |

| Authorised DC master trusts | 33 | ~30m | ~£200bn+ | Dominant growing segment |

Source: TPR Occupational DB Landscape 2025 (December 2025); TPR DC Landscape 2024 (March 2025).

Are UK Workers Saving Enough for Retirement?

The short answer is no — at least not for a significant portion of the working population. The DWP's Analysis of Future Pension Incomes 2025 (published July 2025) found that 43% of working-age individuals — approximately 14.6 million people — are undersaving against their Target Replacement Rate (TRR). For longer-horizon savers weighing options beyond a pension, our comparison of ISA versus pension coverage sits alongside this data.

The adequacy gap is stark when the state pension is compared against PLSA Retirement Living Standards benchmarks. The full new state pension of £11,973 per year in 2025/26 covers just 89% of the PLSA Minimum for a single person — leaving an annual shortfall of approximately £1,427 even at the lowest standard, requiring private savings to bridge the gap.

| PLSA Standard | Single Person | Couple | What It Covers |

|---|---|---|---|

| Minimum | £13,400/yr | £21,600/yr | Basic needs; no car; little social activity |

| Moderate | £31,700/yr | £43,900/yr | Some holidays, car, reasonable social life |

| Comfortable | £43,900/yr | £60,600/yr | Regular holidays, car every 5 years, resilience |

| Full new state pension 2025/26 | £11,973/yr | £23,946/yr (2 pensions) | Exceeds Minimum for couples; short for singles |

Source: PLSA Retirement Living Standards 2025, updated June 2025; DWP Benefit and Pension Rates 2025/26.

| Adequacy Measure | Number of People | % Working-Age Adults |

|---|---|---|

| Undersaving against Target Replacement Rate | 14.6 million | 43% |

| Projected to fall below PLSA Minimum | 4.6 million | 13% |

| Projected to fall below PLSA Moderate | ~24.7 million | 73% |

| Projected to fall below PLSA Comfortable | ~30.9 million | 91% |

| Not currently contributing to any pension | ~13.9 million | 41% |

| No private pension at all | ~6.4 million | 19% |

Source: DWP Analysis of Future Pension Incomes 2025, July 2025; FCA Financial Lives Survey 2024, May 2025.

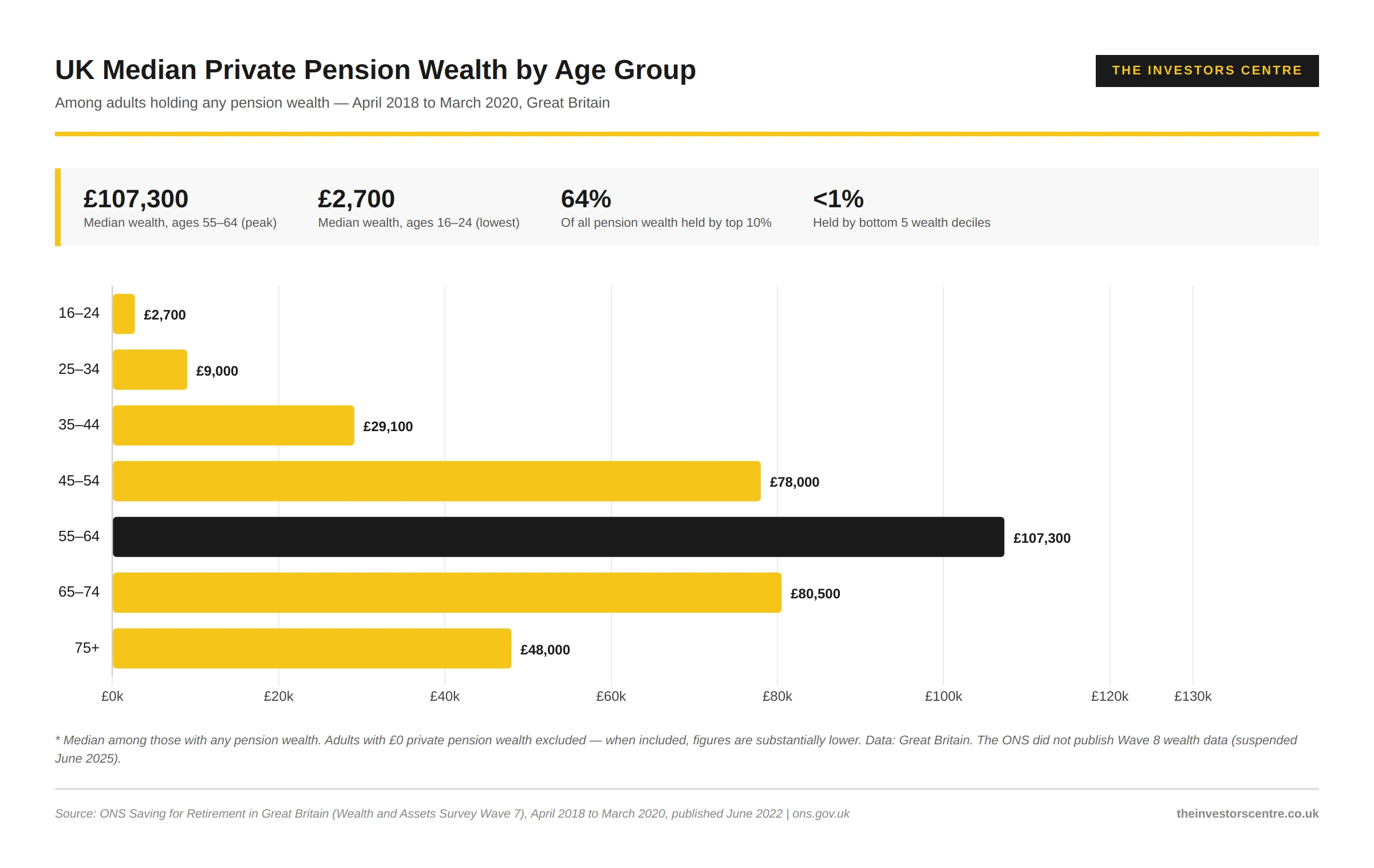

What Is the Average UK Pension Pot Size?

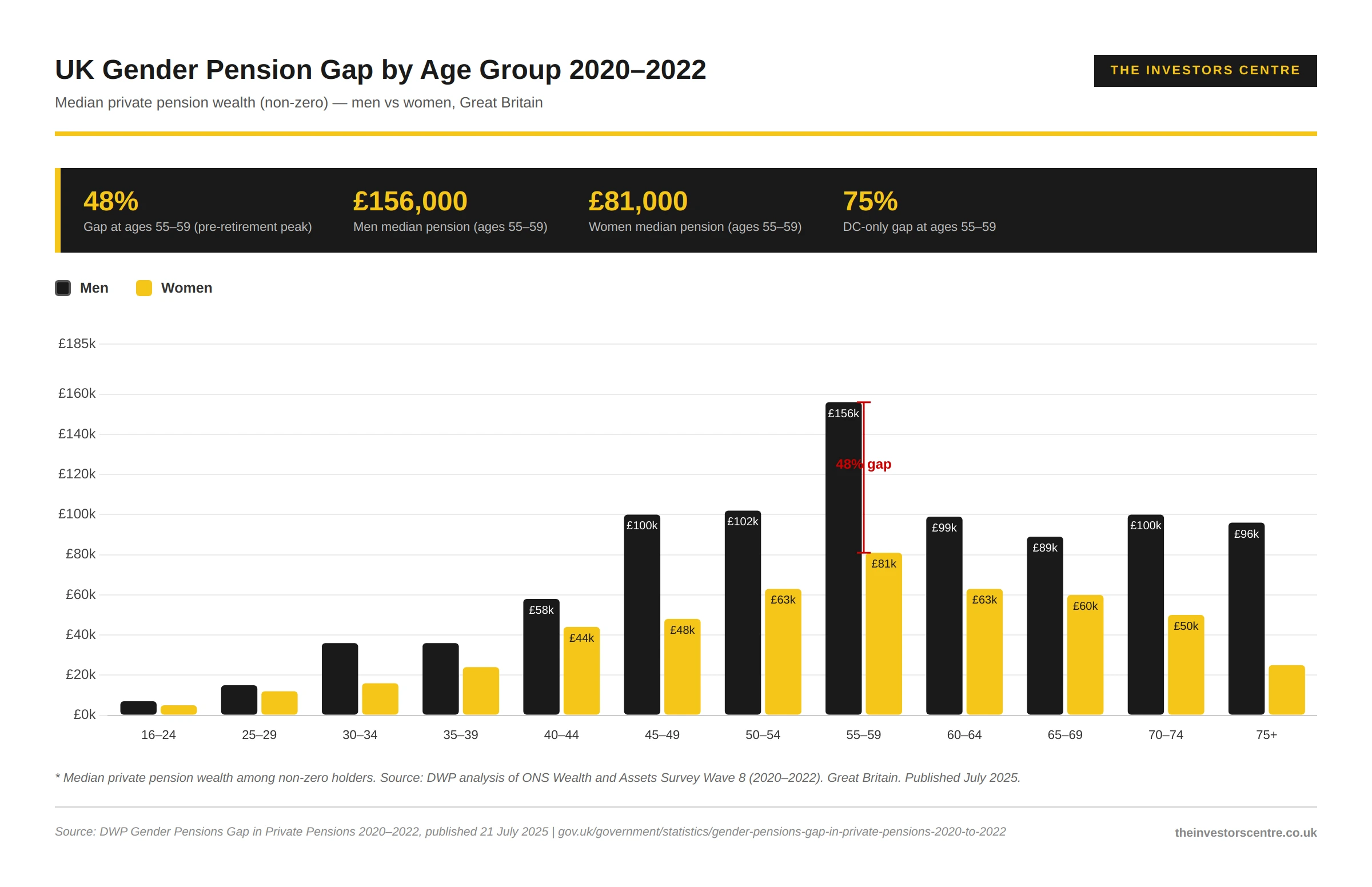

Pension wealth in the UK is highly unequal. The ONS Wealth and Assets Survey (Wave 7, covering April 2018 to March 2020) found that the top 10% of adults held 64% of all private pension wealth, while the bottom 50% of deciles combined held less than 1%. For adults approaching retirement aged 55–59: men hold median private pension wealth of £156,000; women £81,000 — a 48% gap.

| Age Group | Median Pension Wealth (with pension) | % with Private Pension |

|---|---|---|

| 16–24 | £2,700 | 33% |

| 25–34 | £9,000 | 52% |

| 35–44 | £29,100 | 66% |

| 45–54 | £78,000 | 78% |

| 55–64 | £107,300 | 76% |

| 65–74 | £80,500 | 75% |

| 75+ | £48,000 | 70% |

Source: ONS Saving for Retirement in Great Britain (Wealth and Assets Survey, Wave 7), April 2018 to March 2020.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

UK State Pension: Rates, Eligibility and Future Changes

The state pension is the foundation of retirement income for the majority of UK retirees. In 2025/26, the full new state pension pays £230.25 per week (£11,973 per year) — a 4.1% increase under the triple lock guarantee (earnings growth, CPI inflation, or 2.5%, whichever is highest).

| Tax Year | Full New State Pension (Weekly) | Annual | Basic (Old) State Pension | % Increase |

|---|---|---|---|---|

| 2023/24 | £203.85 | £10,600 | £156.20 | 10.1% |

| 2024/25 | £221.20 | £11,502 | £169.50 | 8.5% |

| 2025/26 | £230.25 | £11,973 | £176.45 | 4.1% |

| 2026/27 (forecast) | £241.30 | £12,548 | £184.90 | ~4.8% |

Source: DWP Benefit and Pension Rates 2024/25 and 2025/26; House of Commons Library CBP-10403, 2026.

When Is the State Pension Age Changing?

The state pension age for both men and women rose to 66 in October 2020. The next planned rise — to 67 — begins in April 2026 and will complete by March 2028. A further rise to 68 is legislated for 2044–2046, though this timeline was not brought forward in the 2023 State Pension Age Review.

The Gender Pension Gap: Women Retire with 48% Less Than Men

The UK's gender pension gap is one of the most significant and least-discussed financial inequalities in the country. Among adults aged 55–59, women hold median private pension wealth of £81,000 — just over half the £156,000 held by men in the same age group. This 48% gap measures only those who actually hold pension wealth; when adults with zero pensions are included, the gap widens to 62%.

The DC pension gap (75% for ages 55–59) is far worse than the DB gap (39%), which reflects the fact that DB schemes, with their final salary guarantees and survivor benefits, provide stronger structural protection for lower-earning and part-time workers — who are disproportionately women.

| Gender Pension Gap Metric | Men | Women | Gap |

|---|---|---|---|

| Median pension wealth, 55–59 (non-zero) | £156,000 | £81,000 | 48% |

| Median pension wealth, 55–59 (incl. zero) | £85,000 | £32,000 | 62% |

| Median DC-only wealth, 55–59 | £75,000 | £19,000 | 75% |

| Median DB-only wealth, 55–59 | £183,000 | £111,000 | 39% |

| Average pension wealth at retirement (PPI) | £205,000 | £69,000 | 66% |

Source: DWP Gender Pensions Gap in Private Pensions 2020–2022, July 2025; PPI / NOW: Pensions, February 2024.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

"A 48% gender pension gap at peak pre-retirement age is not a statistical quirk — it is a designed outcome of a system that rewards uninterrupted high-earning careers and makes women's typical career pattern structurally expensive. The DC-only gap of 75% is the more telling figure: the move away from defined benefit to defined contribution has quietly stripped out the one feature of workplace pensions that protected lower-earning, part-time, and career-interrupted workers most."

TIC Analysis: How Much Do You Need to Save to Retire Comfortably?

TIC has calculated the required monthly savings from age 25, 35, and 45 to reach each PLSA Retirement Living Standard at age 67. For readers choosing where to hold retirement assets, our round-up of UK investment platforms covers the major SIPP and pension providers on fees and funds.

| Target Lifestyle | Annual Income Needed | Private Income Gap* | From Age 25 | From Age 35 | From Age 45 |

|---|---|---|---|---|---|

| Minimum (single) | £13,400 | £1,427/yr | ~£15/mo | ~£25/mo | ~£60/mo |

| Moderate (single) | £31,700 | £19,727/yr | ~£215/mo | ~£375/mo | ~£870/mo |

| Comfortable (single) | £43,900 | £31,927/yr | ~£350/mo | ~£605/mo | ~£1,410/mo |

| Moderate (couple, 2 state pensions) | £43,900 | £0 (fully covered) | — | — | — |

| Comfortable (couple, 2 state pensions) | £60,600 | £12,654/yr | ~£70/mo | ~£120/mo | ~£280/mo |

TIC calculation, April 2026.

"The most important number in this whole page is £215 a month — the cost of a moderate single retirement if you start at age 25, versus £870 if you start at 45. Four times the monthly cost for the same outcome. Auto-enrolment's default 8% minimum contribution on average qualifying earnings gets nowhere near that for most workers — which is why the national policy conversation has to move from 'are people saving' to 'are they saving enough'."

Pension Tax Relief: How Much Does It Cost the Government?

The UK Government provides substantial tax relief on pension contributions to incentivise retirement saving. In 2024/25, the estimated total cost of pension tax relief — combining income tax relief and National Insurance contributions relief — is projected at £55.4 billion.

The distribution of tax relief is heavily skewed towards higher earners. Of income tax relief on pension contributions in 2023/24: 55% went to higher rate taxpayers, 32% to basic rate taxpayers, and 13% to additional rate taxpayers. The Annual Allowance — the maximum that can be contributed tax-efficiently each year — rose from £40,000 to £60,000 in April 2023. The Lifetime Allowance was abolished entirely from 6 April 2024.

| Tax Year | Income Tax Relief (£bn) | NICs Relief (£bn) | Total Net Relief (£bn) |

|---|---|---|---|

| 2021/22 | 24.7 | 22.6 | 47.3 |

| 2022/23 | 25.8 | 24.3 | 50.1 |

| 2023/24 | 28.2 | 24.0 | 52.2 |

| 2024/25 (forecast) | 32.3 | 23.1 | 55.4 |

| 2025/26 (forecast) | 33.5 | 25.6 | 59.1 |

Source: HMRC Tax Relief Statistics, January 2026.

What UK Pension Data Tells Us About Retirement Readiness

The headline participation statistics tell one story — auto-enrolment is working, with 89% of eligible employees now saving. But the adequacy data tells quite another: the majority of UK workers are not saving enough to achieve even a moderate retirement lifestyle without significant additional contributions. For the broader retirement context see our TIC investing library.

Three structural problems persist. First, the self-employed pension savings crisis — 20% participation against 80% for employees — represents 4.4 million working adults who are largely invisible to workplace pension policy. Second, the consolidation of the DC market into 33 master trusts creates concentration risk and raises questions about governance quality for the millions of small-balance savers in default funds. Third, the gender pension gap — 48% at peak pre-retirement age — means the UK is systematically producing a generation of women who will be financially dependent in old age. The DWP's own modelling projects that incomes for individuals retiring in 2050 will be only 1% higher in real terms than for those retiring in 2025, and private pension income could actually be 8% lower.

Frequently Asked Questions

How many people have a workplace pension in the UK?

23.3 million employees in the UK were saving into a workplace pension in 2024, representing 82% of all employees and 89% of those who meet auto-enrolment eligibility criteria. Source: DWP, August 2025.

What is the UK state pension in 2025?

The full new state pension is £230.25 per week (£11,973 per year) in 2025/26 — a 4.1% increase under the triple lock. The average amount actually received (including those on the old basic state pension) is £202.62 per week.

How much should I have in my pension by age 50?

There is no single official target, but many financial planners suggest having 10 times your annual salary saved by retirement at 67, implying approximately 5–6 times salary by age 50. The ONS found the median pension wealth for adults aged 45–54 was £78,000 (among those with a pension).

What is the gender pension gap in the UK?

The UK gender pension gap is 48% for adults aged 55–59 — women hold median private pension wealth of £81,000 versus £156,000 for men. The gap is widest in defined contribution schemes (75% gap at 55–59) and narrows in defined benefit schemes (39% gap).

What percentage of UK workers are saving into a pension?

82% of all UK employees were saving into a workplace pension in 2024. Among the 24.4 million who meet auto-enrolment eligibility criteria, 89% were saving. Just 20% of self-employed adults save into a pension.

What is the minimum pension contribution in the UK?

The minimum total pension contribution under auto-enrolment is 8% of qualifying earnings (earnings between £6,240 and £50,270 per year), of which at least 3% must come from the employer. Employees contribute the remaining 5% (typically including tax relief).

How many pension pots are lost in the UK?

An estimated 3.3 million pension pots are lost or unclaimed in the UK, containing approximately £31.1 billion in savings. There are 27.5 million deferred pension pots in total. Source: Pensions Policy Institute Briefing Note 138, October 2024.

What is the average pension pot in the UK at retirement?

There is no single official figure. The ONS Wealth and Assets Survey found median private pension wealth for those approaching retirement (aged 55–59) is £156,000 for men and £81,000 for women among those with any pension wealth. TPR data shows average DC trust-based assets per member of just £7,000, skewed downward by small deferred pots.

When is the state pension age rising to 67?

The state pension age begins rising from 66 to 67 in April 2026 and will complete the transition in March 2028. Anyone born between 6 April 1960 and 5 April 1977 will be affected. A further rise to 68 is legislated for 2044–2046.

What is auto-enrolment?

Auto-enrolment is the system introduced in October 2012 that requires employers to automatically enrol qualifying employees into a workplace pension scheme. Eligible employees (aged 22 to state pension age, earning above £10,000) are enrolled by default. By February 2026, 11.4 million employees had been auto-enrolled who would not otherwise have been saving.

What is the gender pension gap caused by?

The UK gender pension gap is driven by the gender pay gap, career breaks for childcare or caring responsibilities, higher rates of part-time working among women, and occupational segregation into lower-earning sectors. Women face an average 10-year career gap costing approximately £39,000 in lost pension savings.

How much does pension tax relief cost the Government?

The estimated total cost of pension tax relief — combining income tax relief and NICs relief — is £55.4 billion in 2024/25, rising to £59.1 billion in 2025/26. The majority (55%) of income tax relief goes to higher rate taxpayers. Source: HMRC Tax Relief Statistics, January 2026.

What are the PLSA Retirement Living Standards?

PLSA Retirement Living Standards are benchmarks for annual income needed in retirement: Minimum (£13,400/year single; £21,600/year couple), Moderate (£31,700/year single; £43,900/year couple), and Comfortable (£43,900/year single; £60,600/year couple) — updated June 2025.

What percentage of pensioners live in poverty in the UK?

1.9 million pensioners — approximately 16% of the pensioner population — live in relative poverty after housing costs in 2023/24. Women make up 67% of pensioners in poverty. 1.4 million pensioners receive Pension Credit, but up to 760,000 eligible households are not claiming.

What is a defined benefit vs defined contribution pension?

A defined benefit (DB) pension guarantees a specific income in retirement, typically based on salary and years of service. A defined contribution (DC) pension builds up a pot of money based on contributions and investment performance. The UK has seen a major shift from DB to DC: 74% of private sector DB schemes are now closed to future accrual.