- expertise:

- Platform Testing, Cryptocurrency, Retail Investing

- credentials:

- Active investor since 2013 · 11+ years experience

- tested:

- 50+ platforms · 200+ guides authored

- expertise:

- CFD Trading, Forex, Derivatives, Risk Management

- credentials:

- Chartered ACII (2018) · Trading since 2012

- tested:

- 40+ forex & CFD platforms with live accounts

How We Test

Real accounts. Real money. Real trades. No demo accounts or press releases.

What we measure:

- Spreads vs advertised rates

- Execution speed and slippage

- Hidden fees (overnight, withdrawal, conversion)

- Actual withdrawal times

Scoring:

Fees (25%) · Platform (20%) · Assets (15%) · Mobile (15%) · Tools (10%) · Support (10%) · Regulation (5%)

Regulatory checks:

FCA Register verification · FSCS protection

Testing team:

Adam Woodhead (investing since 2013), Thomas Drury (Chartered ACII, 2018), Dom Farnell (investing since 2013) — 50+ platforms with funded accounts

Quarterly reviews · Corrections: in**@*******************co.uk

Disclaimer

Not financial advice. Educational content only. We're not FCA authorised. Consult a qualified advisor before investing.

Capital at risk. Investments can fall. Past performance doesn't guarantee future results.

CFD warning. 67-84% of retail accounts lose money trading CFDs. High risk due to leverage.

Contact: in**@*******************co.uk

Key UK SIPP Statistics 2026

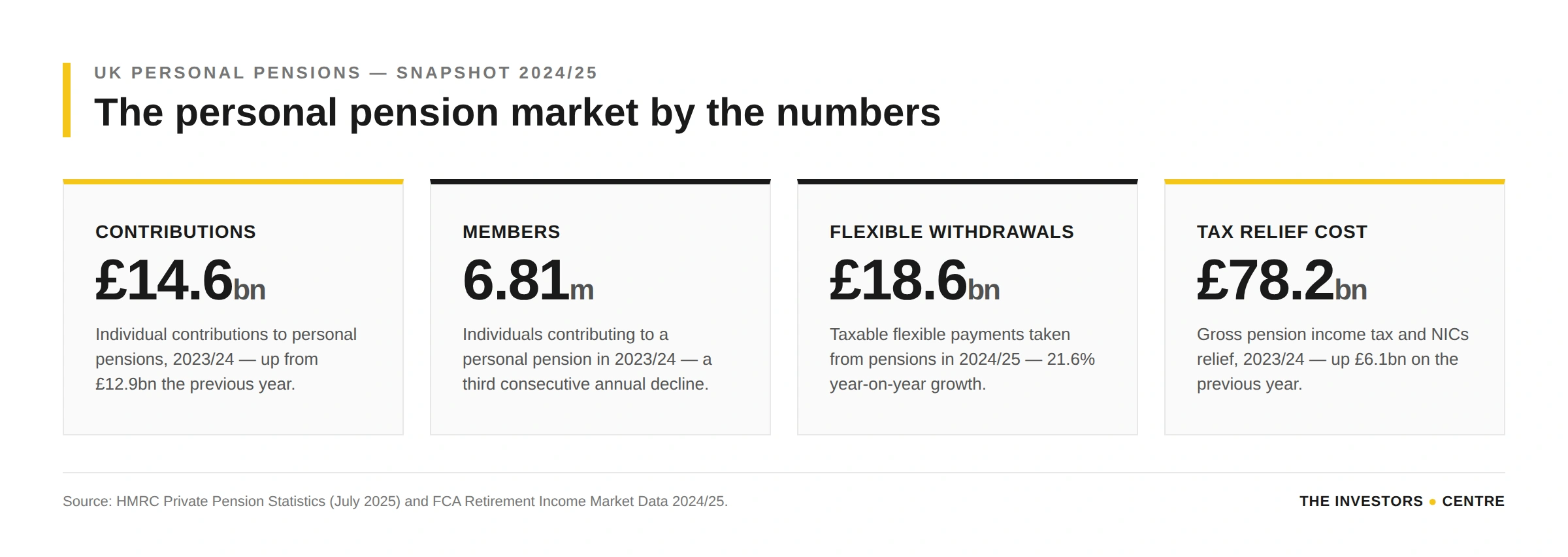

- £14.6 billion of individual contributions were made to UK personal pensions in 2023/24, up from £12.9 billion the previous year.

- 6.81 million people contributed to a personal pension in 2023/24 — a third consecutive annual decline from the 7.44 million peak in 2021/22.

- £2,144 average annual contribution per personal pension member in 2023/24, up 13.6% year-on-year as the member base narrowed.

- £78.2 billion gross pension income tax and NICs relief in 2023/24, rising £6.1 billion in one year.

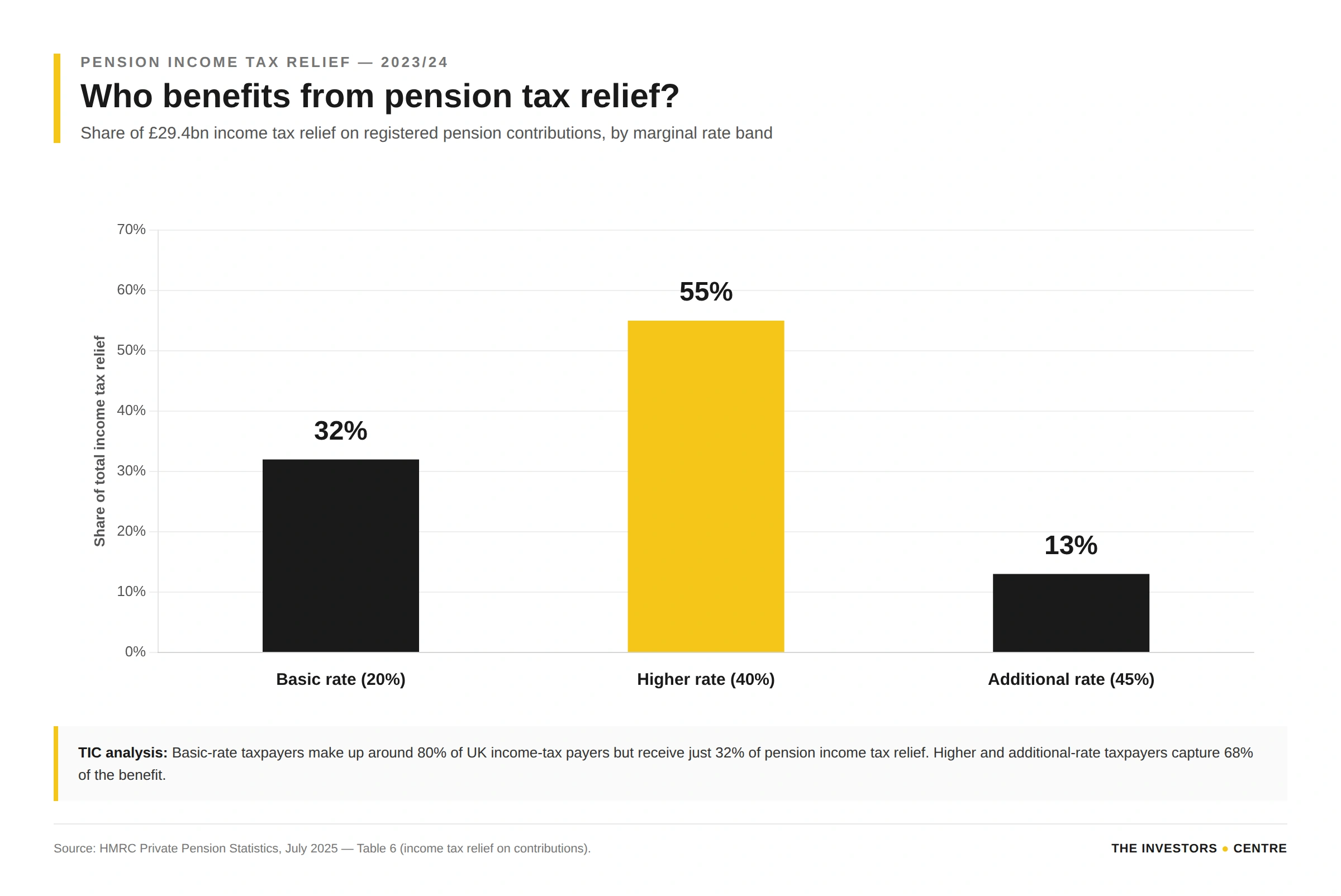

- 55% of pension income tax relief flows to higher-rate taxpayers — only 32% goes to basic-rate taxpayers despite them making up ~80% of the income-tax base.

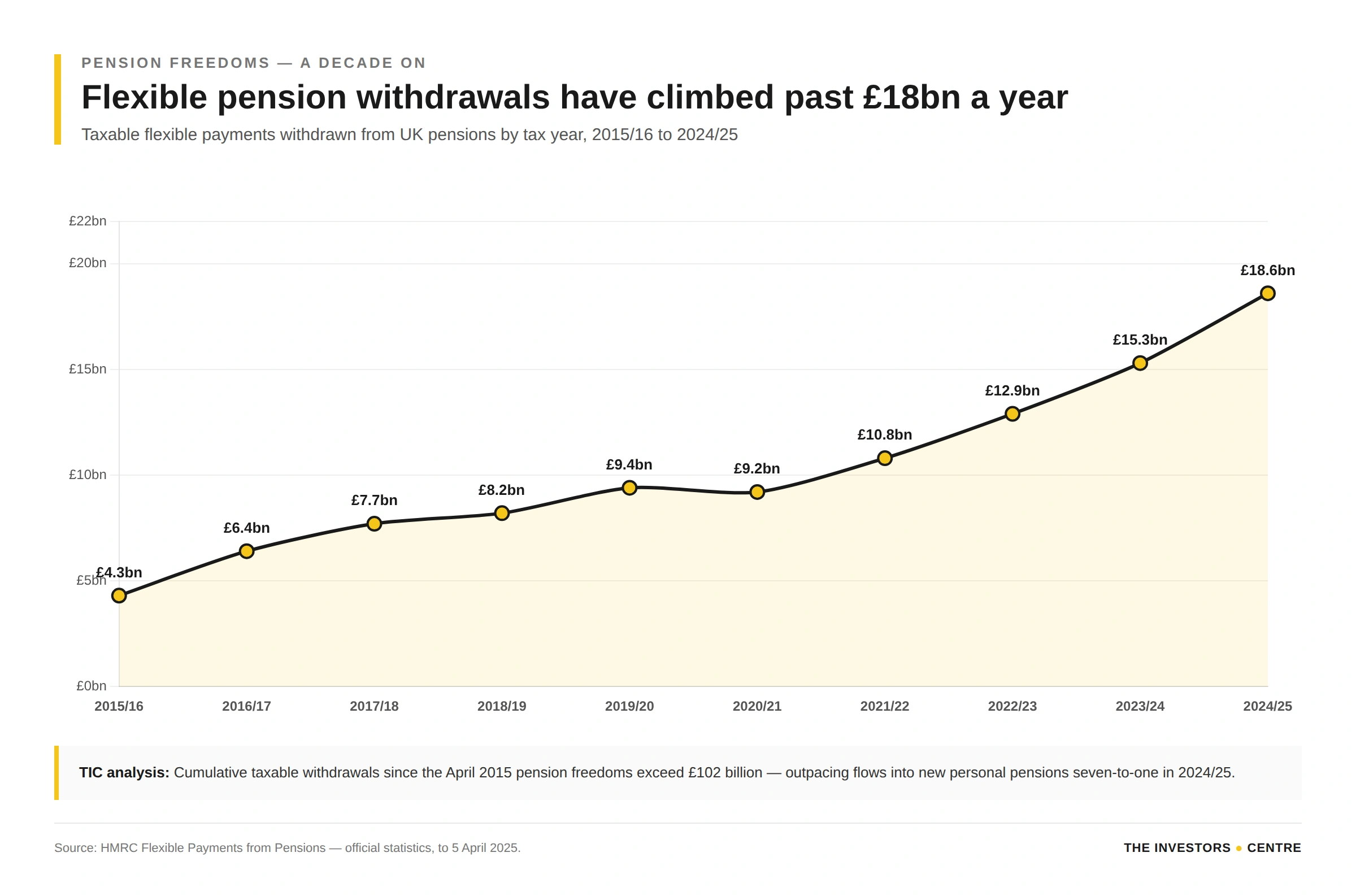

- £18.6 billion taken as taxable flexible payments from UK pensions in 2024/25, a 21.6% year-on-year increase and the highest total since pension freedoms began.

- £102 billion cumulative taxable flexible withdrawals since the April 2015 pension freedoms.

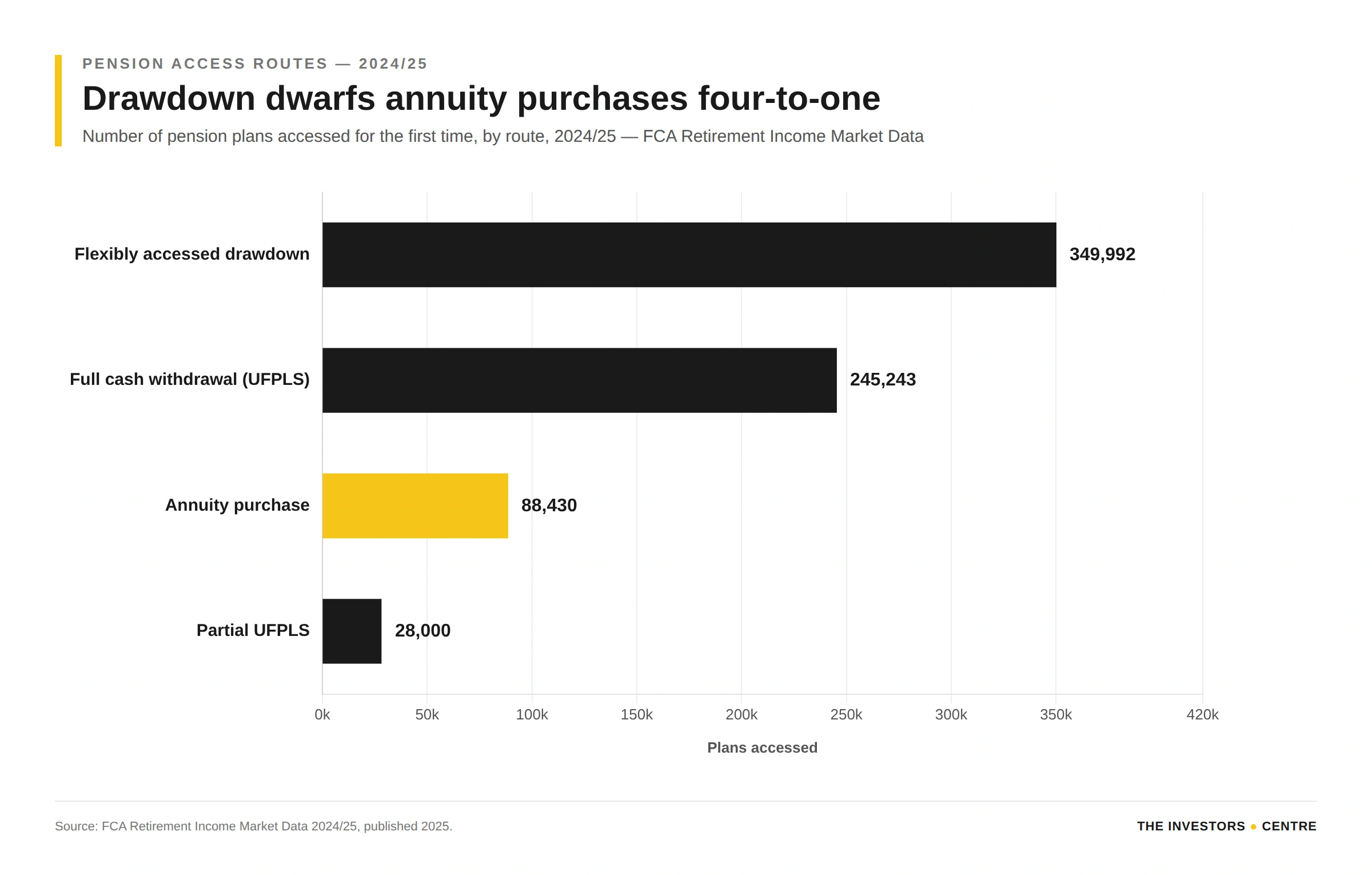

- 4:1 drawdown vs annuity — 349,992 pension plans entered drawdown in 2024/25 versus 88,430 annuity purchases.

- 30.6% of pension plans accessed for the first time in 2024/25 used regulated financial advice — a persistent concern for the FCA.

- 12.5 million UK adults are under-saving for retirement, per FCA estimates in Policy Statement PS25/22 (September 2025).

- 2 million active clients at Hargreaves Lansdown with £172.7 billion AUA (June 2025) — the UK's largest SIPP and investment platform.

- £17.6 million lost to reported UK pension fraud in 2024, averaging £33,848 per victim across 519 Action Fraud reports.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

How Much Is Paid Into UK Personal Pensions Each Year?

UK savers contributed £14.6 billion to personal pensions in 2023/24, up from £12.9 billion in 2022/23. Of this, £2.7 billion came from self-employed members. Contributions have been growing year-on-year even as the number of contributing members has fallen. Personal pensions include SIPPs, stakeholder pensions, and other individually held schemes outside workplace auto-enrolment.

| Tax year | Members contributing | Total contributions | Self-employed contributions | Avg per member |

|---|---|---|---|---|

| 2019/20 | 7.37m | £10.2bn | £1.4bn | £1,383 |

| 2020/21 | 7.30m | £9.4bn | £1.2bn | £1,288 |

| 2021/22 | 7.44m | £10.5bn | £1.6bn | £1,411 |

| 2022/23 | 7.05m | £12.9bn | £2.5bn | £1,830 |

| 2023/24 | 6.81m | £14.6bn | £2.7bn | £2,144 |

Source: HMRC Private Pension Statistics, July 2025. Average per member calculated by The Investors Centre.

The pattern is clear: fewer people are paying into personal pensions, but those who remain are contributing significantly more. Auto-enrolment into workplace pensions absorbs much of the mass-market saving that once flowed through stakeholder products, leaving personal pensions increasingly used by higher earners and the self-employed as a top-up or primary pension wrapper.

UK Pension Tax Relief — Who Benefits and By How Much?

Gross UK pension tax relief cost £78.2 billion in 2023/24, made up of £52.5 billion in income tax relief and £25.7 billion in National Insurance relief via salary sacrifice and employer contributions. Higher-rate taxpayers receive 55% of income tax relief on pension contributions, despite making up a minority of the income-tax base.

| Relief type | 2022/23 | 2023/24 | Change |

|---|---|---|---|

| Income tax relief (gross) | £50.0bn | £52.5bn | +5.0% |

| NICs relief on employer contributions | £22.1bn | £25.7bn | +16.3% |

| Total gross relief | £72.1bn | £78.2bn | +8.5% |

| Income tax on pensions in payment (offset) | £22.6bn | £25.7bn | +13.7% |

| Net cost of pension relief to Exchequer | £49.5bn | £52.5bn | +6.1% |

Source: HMRC Private Pension Statistics, Tables 6 and 7, July 2025.

Only 32% of income tax relief is claimed at the basic rate, even though basic-rate taxpayers account for roughly four in five UK income-tax payers. This concentration is a recurring target of Budget reform speculation.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

How Big Is the UK SIPP Market?

The UK SIPP market is dominated by a small group of scale platforms. Hargreaves Lansdown passed two million active clients in June 2025 with £172.7 billion in assets under administration, up 11% year-on-year, according to its FY25 results. Net new business jumped 43% to £6 billion. Interactive Investor, AJ Bell, Fidelity, and Aviva make up the remainder of the Tier-1 market — see our comparison of leading UK investment and SIPP platforms for a side-by-side benchmark.

A second tier of low-cost challengers is compressing fees. InvestEngine scrapped its 0.15% SIPP platform charge in 2025, making its DIY pension effectively free aside from underlying ETF costs. Moneybox, Penfold, and AJ Bell's Dodl app continue to pull in younger, smaller-balance customers through app-native journeys. JPMorgan Chase has confirmed plans to launch a UK retail investment and pension platform in 2026.

| Platform | Active clients | AUA / AUM | Reporting date |

|---|---|---|---|

| Hargreaves Lansdown | 2,005,000 | £172.7bn | June 2025 |

| Interactive Investor (abrdn) | 450,000+ | £77bn (total platform) | FY 2024 |

| AJ Bell | 593,000 (advised + D2C) | £94.1bn | FY 2024 (Sept 2024) |

| Fidelity Personal Investing | ~300,000 (est.) | £45bn (est.) | 2024 disclosures |

| InvestEngine | 150,000+ | £500m+ | Q1 2025 |

Source: Company results and regulatory disclosures, 2024–2025. SIPP-only figures are not separately disclosed by most platforms.

"The UK SIPP market is now clearly bifurcated: Hargreaves Lansdown at £172.7bn AUA and two million clients is an order of magnitude larger than the nearest challenger, yet InvestEngine's decision to scrap the 0.15% SIPP fee in 2025 tells you where the price pressure actually sits. The next five years of the SIPP market will not be won by brand or research depth — it will be won on all-in cost for a default global-tracker SIPP. JPMorgan Chase's 2026 entry will accelerate that."

How Do UK Savers Access Their Pensions? Drawdown vs Annuity

Drawdown is now the mainstream pension-access route in the UK. In 2024/25, 349,992 pension plans entered flexibly accessed drawdown compared with 88,430 annuity purchases and 245,243 full cash withdrawals (UFPLS). Total pension withdrawals hit £70.9 billion in 2024/25, up 35.9% year-on-year.

The preference for flexibility over guaranteed income holds even with annuity rates at their strongest level in over a decade — typical level rates at ages 65–67 have been in the 7.0–7.5% range in early 2026. Behavioural inertia, distrust of annuity-for-life irreversibility, and the legacy appeal of passing pension wealth on tax-free (a loophole closing in April 2027) have all pushed savers towards drawdown.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

UK Flexible Pension Withdrawals — A Decade of Pension Freedoms

Since George Osborne's April 2015 pension freedoms, UK savers have taken cumulative taxable flexible withdrawals exceeding £102 billion. In 2024/25 alone the total was £18.6 billion, up from £15.3 billion the year before — the biggest single-year jump since the reforms began.

| Tax year | Taxable flexible withdrawals | Individuals withdrawing | Avg per withdrawer |

|---|---|---|---|

| 2015/16 | £4.3bn | 230,000 | £18,700 |

| 2017/18 | £7.7bn | 415,000 | £18,550 |

| 2019/20 | £9.4bn | 560,000 | £16,786 |

| 2021/22 | £10.8bn | 705,000 | £15,319 |

| 2022/23 | £12.9bn | 780,000 | £16,538 |

| 2023/24 | £15.3bn | 885,000 | £17,288 |

| 2024/25 | £18.6bn | 1,010,000 | £18,416 |

Source: HMRC Flexible Payments from Pensions, official statistics to 5 April 2025. Individuals and averages are TIC estimates derived from HMRC release data.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

TIC Analysis: The SIPP Million Projection

Our analysis shows that a UK saver funding a SIPP at the 2023/24 average contribution rate (£2,144 annually), with basic-rate tax relief grossing this up to £2,680, would accumulate approximately £326,000 over 40 years assuming a 5% real annual return. To reach £1 million in the same timeframe, annual gross contributions would need to average £8,220 — close to the full basic-rate threshold used by higher earners but well above the typical member contribution. If you are deciding whether to prioritise a pension or a stocks and shares ISA, the numbers below are a good starting benchmark.

| Annual gross contribution | 20 years @ 5% | 30 years @ 5% | 40 years @ 5% |

|---|---|---|---|

| £2,680 (2023/24 avg, incl. 20% relief) | £92,700 | £186,300 | £326,000 |

| £5,000 | £173,000 | £348,000 | £608,000 |

| £8,220 | £284,500 | £572,000 | £1,000,000 |

| £10,000 | £346,000 | £697,000 | £1,217,000 |

| £20,000 | £693,000 | £1,393,000 | £2,434,000 |

| £60,000 (max annual allowance) | £2,078,000 | £4,180,000 | £7,303,000 |

TIC calculation, April 2026.

UK Pension Fraud Statistics

UK pension fraud cost savers £17.6 million in 2024 across 519 reports to Action Fraud, averaging £33,848 per victim. The figure is broadly flat on 2023's £17.75 million from 559 reports. The Pensions Regulator's Pension Scams Action Group identifies 50–69 year-olds as the highest-risk cohort, and AI-enabled impersonation plus account takeover as the fastest-growing attack vectors.

Every pre-Budget rumour cycle around the pension tax-free lump sum triggers a surge in scam activity — fraudsters pose as advisers offering to "protect" savings from imminent Treasury changes. The 60% rise in flexible lump-sum withdrawals since 2022 has also enlarged the attack surface.

What Changes When Pensions Fall Into Inheritance Tax in April 2027?

From 6 April 2027, most unused UK pension funds and pension death benefits will be included in the deceased's estate for inheritance tax purposes — ending a regime that made pensions a near-perfect intergenerational wealth-transfer wrapper. HM Treasury estimates around 10,500 estates a year will face a new IHT charge as a result, out of roughly 213,000 estates with pension wealth.

| Element | Pre-April 2027 | From 6 April 2027 |

|---|---|---|

| IHT on unused pension at death | Generally outside estate | Included in estate for IHT |

| Combined tax on pension death benefits (age 75+, 40% IHT + 45% income tax) | ~45% | Up to ~67% |

| Spouse / civil-partner bequest | Exempt | Exempt (unchanged) |

| Registered charity bequest | Exempt | Exempt (unchanged) |

| Affected estates per year (HMT estimate) | n/a | ~10,500 |

Source: HM Treasury draft Finance Bill 2025-26 (July 2025); The Private Office / Royal London 2025.

UK Retirement Under-Saving — The Mass-Market Reality

The FCA's Financial Lives 2024 survey found that roughly one-third of UK adults with a defined contribution pension hold less than £10,000 in total DC pension wealth — see our dataset on how much UK savers typically hold in their pension pots for the full distribution. The FCA's September 2025 Policy Statement PS25/22 cites 12.5 million adults as under-saving for retirement on current trajectories.

PS25/22 introduces "targeted support" as a new FCA-specified activity — a regime designed to let platforms and providers issue firm-led nudges that fall short of full regulated advice. This matters for SIPP providers: the new rules, coming into force in 2026, could legitimise platform guidance to the 45+ cohort with no clear decumulation plan, potentially reshaping the commercial model for mass-affluent pension services.

"30.6% of first-time pension accessors took regulated advice in 2024/25 — the inverse is that nearly 70% made decumulation decisions with Pension Wise guidance, information-only support, or no professional input at all. When drawdown beats annuity four-to-one and withdrawals jump 35.9% in a single year, the absence of advice is not a minor concern: it's the single biggest outstanding consumer protection gap in UK pensions. PS25/22's targeted support regime is the closest thing to a fix currently on the statute book."

Frequently Asked Questions

How many SIPPs are there in the UK?

UK SIPP-specific member counts are not published by HMRC, but total personal pension membership (including SIPPs, stakeholder pensions, and other individual schemes) was 6.81 million in 2023/24. Hargreaves Lansdown alone serves over two million clients, most of whom hold a SIPP.

What is the average UK SIPP contribution?

The average annual contribution per personal pension member in 2023/24 was £2,144, up from £1,830 the previous year. SIPP-specific averages are typically higher on engaged platforms.

How much flexible pension income was withdrawn in 2024/25?

UK savers withdrew £18.6 billion in taxable flexible pension payments in 2024/25, up from £15.3 billion the year before. Cumulative withdrawals since April 2015 now exceed £102 billion.

How many UK savers buy an annuity instead of using drawdown?

In 2024/25, 88,430 pension plans were used to buy an annuity compared to 349,992 entering drawdown — a ratio of roughly one annuity for every four drawdown conversions.

What is the UK pension annual allowance in 2026?

The standard pension annual allowance is £60,000 in 2025/26 and 2026/27, unchanged since it rose from £40,000 in April 2023. High earners may be subject to a tapered allowance down to £10,000, and those who have flexibly accessed a pension trigger the MPAA of £10,000.

Has the lifetime allowance been abolished?

Yes. The pension lifetime allowance was set to zero for 2023/24 and fully abolished from April 2024. It has been replaced by the Lump Sum Allowance (£268,275) and the Lump Sum and Death Benefit Allowance (£1,073,100).

Will my SIPP be subject to inheritance tax?

From 6 April 2027, most unused pension funds — including SIPPs — will be included in the deceased's estate for inheritance tax purposes. Spouse and civil-partner bequests remain exempt. HM Treasury estimates around 10,500 estates a year will face a new IHT charge.

How much tax relief does the UK government provide on pension contributions?

Gross pension tax and NICs relief totalled £78.2 billion in 2023/24. After income tax on pensions in payment, the net cost to the Exchequer is around £52.5 billion per year.

Who benefits most from UK pension tax relief?

Higher-rate taxpayers receive 55% of income tax relief on pension contributions, basic-rate 32%, and additional-rate 13%. The concentration at the top reflects higher earners' greater ability to contribute and their larger marginal-rate top-up.

What is the biggest UK SIPP provider?

Hargreaves Lansdown is the largest, with 2 million active clients and £172.7 billion in assets under administration as of June 2025. AJ Bell, Interactive Investor, Fidelity, and Aviva are the other Tier-1 providers by scale.

Are SIPP fees coming down?

Yes. InvestEngine scrapped its 0.15% SIPP platform fee in 2025, and new entrants including JPMorgan Chase are expected to launch low-cost UK pension offerings in 2026.

How many people take regulated advice when accessing their pension?

Only 30.6% of pension plans accessed for the first time in 2024/25 used regulated financial advice. The remaining 69.4% either used Pension Wise guidance, made decisions without professional input, or received non-regulated support.

How big is UK pension fraud?

Action Fraud recorded 519 pension fraud reports in 2024 totalling £17.6 million, averaging £33,848 per victim. Losses are broadly flat year-on-year but the true scale may be understated.

How many UK adults are under-saving for retirement?

The FCA estimates around 12.5 million UK adults are under-saving for retirement, per Policy Statement PS25/22 (September 2025). Approximately one-third of UK DC pension holders have less than £10,000 in pension wealth.

What is targeted support and how does it affect SIPPs?

Targeted support is a new FCA-specified activity introduced in PS25/22 (2025) and coming into force in 2026. It allows pension providers and platforms to give firm-led nudges to customers — falling short of full regulated advice — which is expected to reshape how SIPP providers engage with under-saving and decumulation-ready customers.