- expertise:

- Platform Testing, Cryptocurrency, Retail Investing

- credentials:

- Active investor since 2013 · 11+ years experience

- tested:

- 50+ platforms · 200+ guides authored

- expertise:

- CFD Trading, Forex, Derivatives, Risk Management

- credentials:

- Chartered ACII (2018) · Trading since 2012

- tested:

- 40+ forex & CFD platforms with live accounts

How We Test

Real accounts. Real money. Real trades. No demo accounts or press releases.

What we measure:

- Spreads vs advertised rates

- Execution speed and slippage

- Hidden fees (overnight, withdrawal, conversion)

- Actual withdrawal times

Scoring:

Fees (25%) · Platform (20%) · Assets (15%) · Mobile (15%) · Tools (10%) · Support (10%) · Regulation (5%)

Regulatory checks:

FCA Register verification · FSCS protection

Testing team:

Adam Woodhead (investing since 2013), Thomas Drury (Chartered ACII, 2018), Dom Farnell (investing since 2013) — 50+ platforms with funded accounts

Quarterly reviews · Corrections: in**@*******************co.uk

Disclaimer

Not financial advice. Educational content only. We're not FCA authorised. Consult a qualified advisor before investing.

Capital at risk. Investments can fall. Past performance doesn't guarantee future results.

CFD warning. 67-84% of retail accounts lose money trading CFDs. High risk due to leverage.

Contact: in**@*******************co.uk

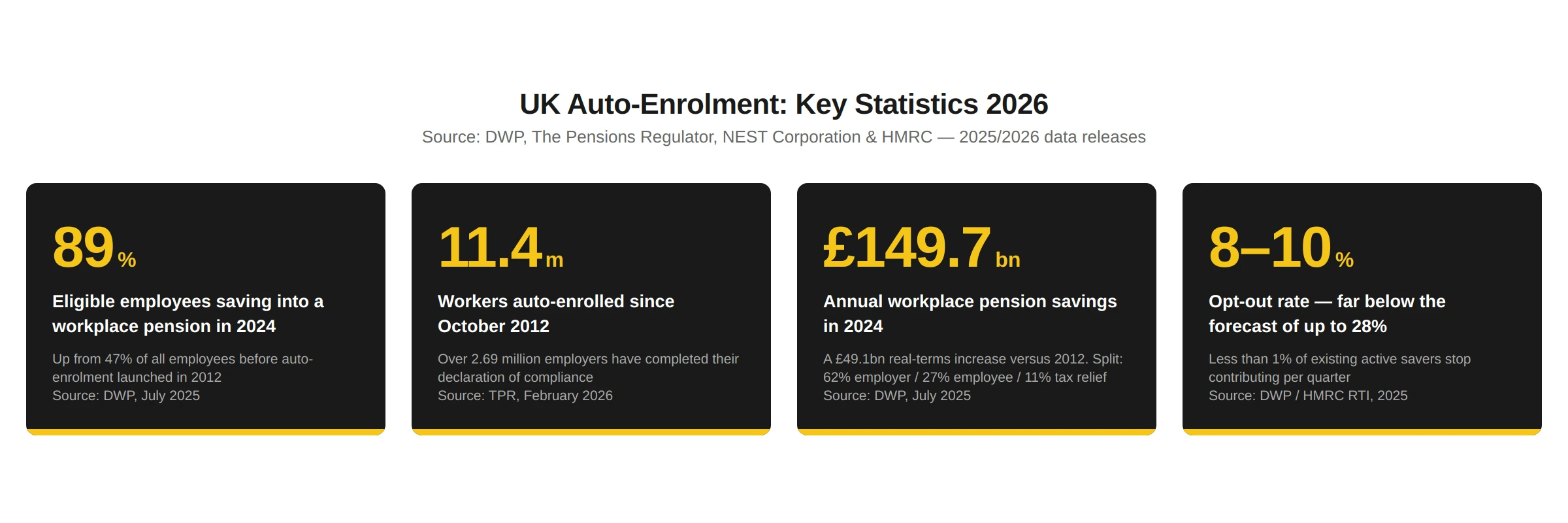

Key Auto-Enrolment Statistics at a Glance

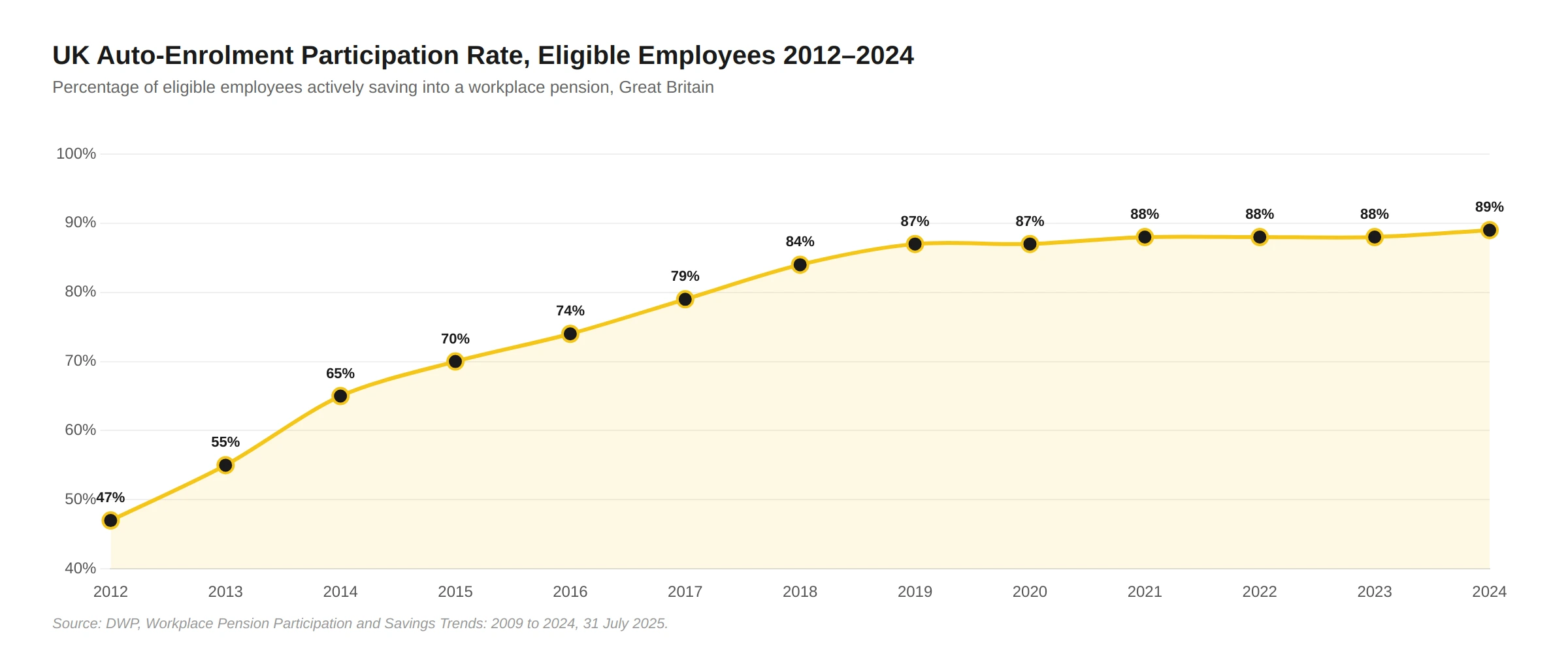

- 89% of eligible employees in the UK were saving into a workplace pension in 2024 — up from just 47% of all employees before auto-enrolment launched.

- 11.4 million workers have been automatically enrolled into a workplace pension since the scheme launched in October 2012 — the largest expansion of pension saving in UK history.

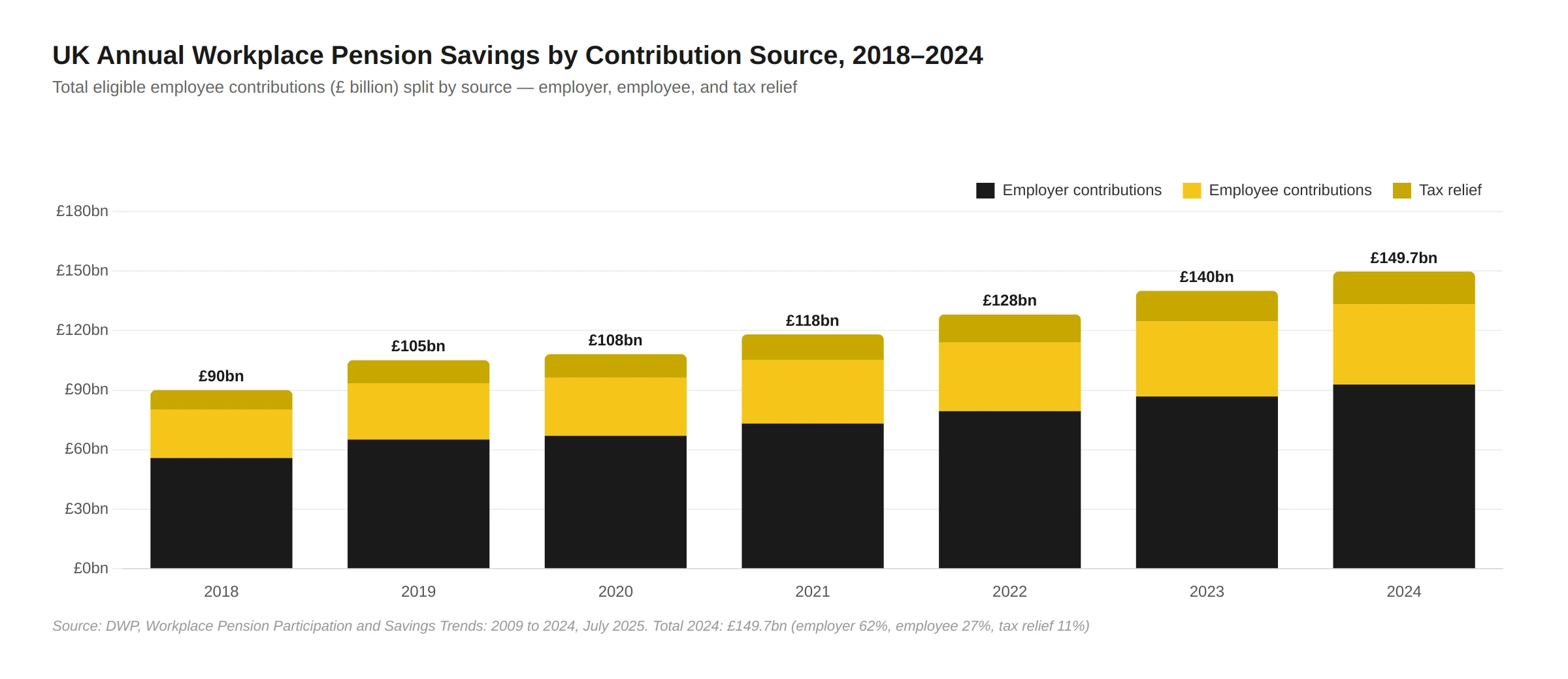

- £149.7 billion flows into UK workplace pensions each year as of 2024 — a real-terms increase of £49.1 billion compared to 2012.

- 2,693,697 employers have completed their auto-enrolment declaration of compliance as of February 2026, covering over 36 million workers.

- 8–10% opt-out — rates have remained between 8% and 10%, far below the government's original forecast of up to 28%.

- NEST: 13.8 million members and £49.7 billion AUM as of March 2025 — with NEST's first-ever annual profit of £11.9 million.

- 22% of self-employed workers earning over £10,000 were saving into a private pension in 2022 — leaving an estimated 3.5 million people building no private pension at all.

- 43% undersaving — approximately 14.6 million working-age people are currently undersaving for retirement against target replacement rates.

- Extension Act 2023 — the Pensions (Extension of Automatic Enrolment) Act 2023 would lower eligibility from 22 to 18 and remove the Lower Earnings Limit. No regulations introduced as of April 2026.

- £136,000 gender gap — women retire with average pension savings of £69,000 versus men's £205,000. 79% of all workers earning below the £10,000 auto-enrolment trigger are women.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

How Many People Are Auto-Enrolled in the UK?

In 2024, 21.7 million eligible UK employees were actively saving into a workplace pension — up 800,000 from the previous year, and representing 89% of all eligible employees in Great Britain. Across all employees (including those below the earnings threshold or aged under 22), 23.3 million workers were saving into a workplace pension in 2024, representing an overall participation rate of 82% — the highest on record. For the broader pension context see our UK pension statistics dataset.

| Year | Eligible Employee Participation | Employees Actively Saving |

|---|---|---|

| 2012 (pre-launch) | ~47% (all employees) | ~10.7 million |

| 2014 | ~65% | c.12.5 million |

| 2016 | ~74% | c.15.0 million |

| 2018 | ~84% | c.17.8 million |

| 2019 | ~87% | c.18.7 million |

| 2021 | ~88% | 20.0 million |

| 2022 | ~88% | 20.5 million |

| 2023 | ~88% | 20.9 million |

| 2024 | 89% | 21.7 million |

Source: DWP, Workplace Pension Participation and Savings Trends: 2009 to 2024, 31 July 2025.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

How Many Employers Have Complied With Auto-Enrolment?

As of February 2026, 2,693,697 UK employers have completed their declaration of compliance with auto-enrolment, covering a total of 36.3 million workers across those declaring employers. A further 1,548,611 employers have completed their re-declaration of compliance — the three-yearly re-enrolment process. The Pensions Regulator has exercised cumulative enforcement powers over one million times since 2012.

| TPR Compliance Metric | Figure (February 2026) |

|---|---|

| Total employers completed declaration | 2,693,697 |

| Total workers at declaring employers | 36.3 million |

| Workers actively in qualifying scheme | 23.7 million |

| Employers completed re-declaration | 1,548,611 |

| Workers re-enrolled after opt-out | 1,071,000 |

| Cumulative AE enforcement actions | Over 1,017,363 |

Source: The Pensions Regulator, Automatic Enrolment Declaration of Compliance Report, February 2026.

What Is the Auto-Enrolment Opt-Out Rate?

Approximately 8–10% of newly enrolled workers opt out of auto-enrolment each year — far below the government's original modelled forecast of up to 28%. The opt-out rate increased modestly during the cost-of-living crisis, reaching approximately 10.4% in 2022, before settling back to around 9.9–10% by late 2024.

The proportion of existing active savers who stop saving each quarter has remained below 1% and barely changed even during the cost-of-living crisis. HMRC Real-Time Information data shows the cessation rate moved from just 0.49% in January 2020 to 0.57% in August 2022 — a remarkably small shift. Despite this aggregate resilience, the FCA Financial Lives Survey 2024 found that 4% of all UK adults stopped contributing to a pension in the 12 months to May 2024 specifically to make ends meet — rising to 12% among the self-employed.

"The single most underrated fact about UK auto-enrolment is that the opt-out rate came in at less than half the government's original forecast — and stayed there through a cost-of-living crisis, two recessions, and a decade of real wage stagnation. Inertia, as behavioural economics predicted, beats rational calculation almost every time. That is why the next reform lever is contribution rates, not participation — the nudge architecture already works."

How Much Is Saved Into Auto-Enrolment Pensions Each Year?

Total annual workplace pension savings for eligible employees reached £149.7 billion in 2024 — a £49.1 billion real-terms increase compared to 2012. The contribution split in 2024 was: employer contributions 62%, employee contributions 27%, and income tax relief 11%.

| Period | Employer Minimum | Employee Minimum | Total Minimum |

|---|---|---|---|

| Oct 2012 – Apr 2018 | 1% | 1% | 2% |

| Apr 2018 – Apr 2019 | 2% | 3% | 5% |

| Apr 2019 – present | 3% | 5% | 8% |

Source: DWP / The Pensions Regulator. Percentages apply to qualifying earnings (currently £6,240–£50,270).

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

NEST: The UK's Largest Auto-Enrolment Pension Scheme

NEST (National Employment Savings Trust) is the UK government-backed workplace pension scheme designed to ensure every employer has access to a qualifying scheme. It serves as the default for the majority of the UK's smallest businesses — 98% of NEST employers have fewer than 50 employees.

| NEST Metric | March 2022 | March 2023 | March 2024 |

|---|---|---|---|

| Total members | 11.1m | 12.0m | 13.0m |

| Assets under management | £24.4bn | £29.6bn | £40.6bn |

| Monthly contributions | £477m | £543m | £605m |

| Annual profit / (loss) | (Loss) | (Loss) | (Loss) |

Source: NEST Corporation Annual Reports. March 2025: 13.8m members, £49.7bn AUM, £663m/month contributions, first-ever profit of £11.9m.

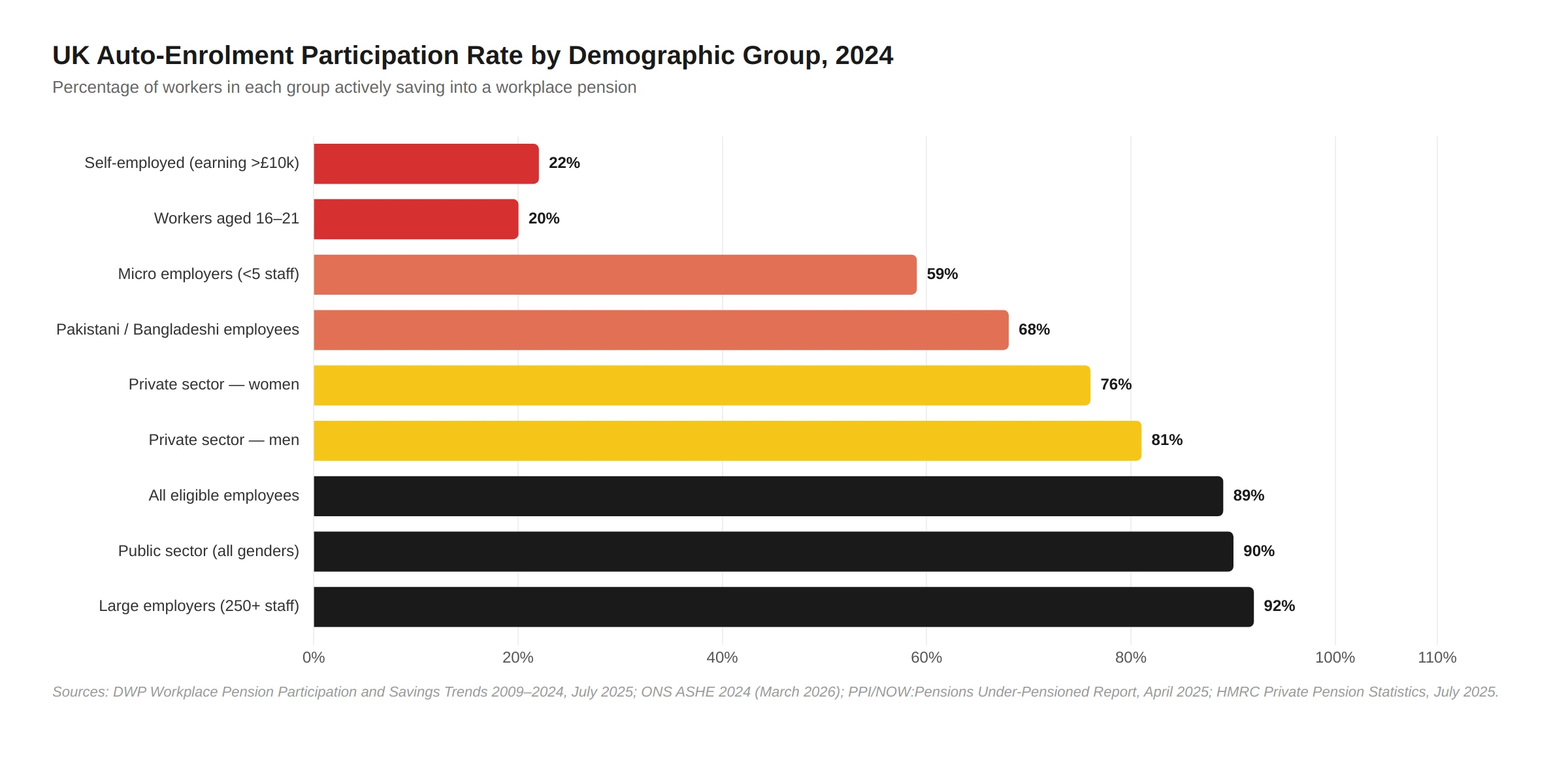

Auto-Enrolment Participation by Gender, Age and Employer Size

Auto-enrolment has not produced uniform outcomes across all groups. A gender gap persists in the private sector: 81% of men versus 76% of women participated in 2024. In the public sector, participation was equal at 90% for both genders — driven by the dominance of defined benefit schemes.

| Demographic Group | Participation Rate (2024) |

|---|---|

| All eligible employees | 89% |

| Private sector — men | 81% |

| Private sector — women | 76% |

| Public sector — both genders | 90% |

| Workers aged 22–State Pension age | ~80% |

| Workers aged 16–21 (below threshold) | ~20% |

| Micro employers (<5 staff) | ~59% |

| Large employers (250+ staff) | Over 90% |

| Pakistani / Bangladeshi eligible employees | ~68% |

| Self-employed earning over £10,000 | 22% |

Source: DWP, July 2025; ONS ASHE 2024; DWP Family Resources Survey.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

The Auto-Enrolment Gender Pension Gap

Auto-enrolment has narrowed but not closed the gender pension gap. Women retire with average pension savings of £69,000 compared to £205,000 for men — a £136,000 gap. The PPI and NOW:Pensions estimate that women would need to work an extra 19 years to close this gap. The structural cause lies partly in auto-enrolment's design: the £10,000 earnings trigger excludes workers whose earnings fall below this threshold, and 79% of sub-threshold workers are women. Many women working part-time hold multiple jobs each below the threshold, making them ineligible despite meaningful combined earnings. 1.9 million women in the UK earn below the £10,000 auto-enrolment earnings trigger.

The Self-Employed Pension Gap: 3.5 Million People Excluded

Auto-enrolment does not cover the self-employed. Of approximately 3.9 million self-employed workers in the UK, only an estimated 360,000 contributed to a personal pension in 2023/24 — just 22% of those earning over £10,000. This compares to 60% of self-employed workers who saved into a pension in 1998. Self-employed readers looking to start a pension can compare provider fees across our round-up of the major UK investment platforms that offer SIPPs.

The IFS projects that approximately 55% of self-employed workers will have no pension savings to supplement their state pension in retirement.

Are Auto-Enrolment Contributions Enough?

Participation is only half the story. A growing body of evidence from DWP, the PPI, and independent economists concludes that the 8% minimum auto-enrolment contribution rate is insufficient for adequate retirement incomes.

| Adequacy Statistic | Figure & Source |

|---|---|

| Working-age people undersaving (DWP, 2025) | 43% — approximately 14.6 million |

| Projected below PLSA Minimum standard | 4.6 million (13%) |

| Projected below PLSA Comfortable standard | 91% (31.5 million) |

| DC pension holders who say pension alone insufficient | 61% (FCA Financial Lives 2024) |

| Estimated uplift from raising minimum to 12% | +£10bn/year (Phoenix Group, 2024) |

| Extra pot from 8%→12% for an 18-year-old | ~£96,000 (Phoenix Group, 2024) |

Source: DWP Analysis of Future Pension Incomes 2025; FCA Financial Lives Survey 2024; Phoenix Group/WPI Economics, 2024.

Auto-Enrolment Reform: The 2023 Act and What Comes Next

The Pensions (Extension of Automatic Enrolment) Act 2023 received Royal Assent on 18 September 2023. It grants the Secretary of State powers to: (1) lower the minimum eligible age from 22 to 18, and (2) remove the Lower Earnings Limit, so contributions are calculated from the first pound of earnings rather than from £6,240.

| Reform Element | Detail |

|---|---|

| Pensions (Extension of AE) Act 2023 — Royal Assent | 18 September 2023 |

| Eligible age reduction: 22 → 18 | Powers granted; no regulations (April 2026) |

| Removal of Lower Earnings Limit (£6,240) | Powers granted; no regulations (April 2026) |

| DWP estimated additional workers (2017) | ~900,000 — predominantly young / part-time |

| DWP estimated additional annual contributions | ~£3.8 billion |

| Current earnings trigger | £10,000 (frozen since 2014/15) |

| Current Lower Qualifying Earnings Limit | £6,240 |

| Current Upper Qualifying Earnings Limit | £50,270 |

Source: Pensions (Extension of Automatic Enrolment) Act 2023; House of Commons Library SN06417, 19 January 2026; DWP Threshold Review 2026/27, December 2025.

Auto-Enrolment and Pension Tax Relief

Auto-enrolment is substantially funded by tax relief. HMRC's Private Pension Statistics (July 2025, covering 2023/24) show a total gross cost of pension income tax and NICs relief of £78.2 billion, with a net Exchequer cost of £52.5 billion after accounting for income tax paid on pensions in payment. The DWP estimates that auto-enrolment specifically generates approximately £2 billion in additional annual tax relief on employee contributions.

Higher earners receive a disproportionate share of pension tax relief: higher rate taxpayers (40%) receive 55% of all income tax relief on pension contributions, compared to 32% for basic rate taxpayers (20%).

TIC Analysis: The Self-Employed Auto-Enrolment Exclusion Cost

This analysis is original TIC research based on HMRC and ONS data and does not exist elsewhere. It estimates the annual pension contributions being foregone because the self-employed are excluded from auto-enrolment.

| TIC Calculation Input | Figure & Source |

|---|---|

| Total self-employed workers (UK) | ~3.9 million (ONS LFS Q4 2024) |

| Self-employed contributing to pension | ~360,000 (HMRC, July 2025) |

| Estimated non-saving self-employed | ~3,540,000 (TIC calculation) |

| Median self-employed earnings | ~£15,000 (ONS ASHE 2024) |

| AE total minimum contribution rate applied | 8% of qualifying earnings >£6,240 |

| Estimated annual foregone contribution per worker | ~£1,200 |

| TOTAL estimated annual foregone contributions | ~£4.25 billion |

TIC calculation, April 2026. Conservative — excludes employer contributions that would apply if the self-employed were in scope.

"£4.25 billion a year in foregone pension contributions is the price the UK pays for designing auto-enrolment around an employer/employee contract that 3.9 million self-employed workers don't have. Any serious reform that extends participation to the next cohort without an employer in the loop — whether via the tax system, NI credits or a NEST opt-in default — would be the single highest-impact pension policy available between now and 2030. The political work is building consensus on who pays the 'employer' contribution equivalent. See the broader dataset in our TIC investing library."

Frequently Asked Questions: Auto-Enrolment Statistics UK

What is auto-enrolment and when did it start?

Auto-enrolment is the UK government policy that requires employers to automatically enrol eligible workers into a workplace pension scheme. It launched in October 2012, starting with the largest employers, and was fully extended to all employers by 2018.

How many people have been auto-enrolled in the UK?

A total of 11.4 million workers have been automatically enrolled since the scheme launched in October 2012, according to TPR's Declaration of Compliance Report for February 2026. In 2024, 21.7 million eligible employees were actively saving.

What is the auto-enrolment opt-out rate?

Approximately 8–10% of newly enrolled workers opt out of auto-enrolment — consistently far below the government's original forecast of up to 28%. The rate rose slightly to around 10.4% during the cost-of-living crisis in 2022 before settling back.

What percentage of eligible employees are enrolled?

In 2024, 89% of eligible employees in Great Britain were saving into a workplace pension, up from 47% of all employees before auto-enrolment launched. Among all employees (including those not eligible), the participation rate was 82%.

What is the auto-enrolment earnings trigger for 2026?

The auto-enrolment earnings trigger for 2026/27 remains at £10,000 — the same threshold that has applied since 2014/15. Workers earning below this amount are not automatically enrolled, though they may opt in voluntarily.

What are the minimum auto-enrolment contribution rates?

The current minimum total auto-enrolment contribution rate is 8% of qualifying earnings, comprising at least 3% from the employer and 5% from the employee (including tax relief). These rates have applied since April 2019.

Who is excluded from auto-enrolment?

Self-employed workers are entirely excluded from auto-enrolment, as are employees under 22 or over State Pension age, and workers earning below the £10,000 trigger. Workers in multiple jobs can be excluded if each job pays below the threshold.

How much is saved into auto-enrolment pensions each year?

£149.7 billion was saved into UK workplace pensions in 2024, split 62% from employers, 27% from employees, and 11% from income tax relief. This represents a real-terms increase of £49.1 billion compared to 2012.

What is NEST and how many members does it have?

NEST (National Employment Savings Trust) is the UK government-backed workplace pension scheme. As of March 2025, it had 13.8 million members, £49.7 billion AUM, and received average monthly contributions of £663 million. In 2024/25 it recorded its first-ever annual profit of £11.9 million.

What is the gender pension gap in auto-enrolment?

Women retire with average pension savings of £69,000 versus men's £205,000 — a £136,000 gap. In the private sector, 81% of men participated in auto-enrolment in 2024 versus 76% of women. 79% of all workers earning below the £10,000 threshold are women.

What is the Pensions (Extension of Automatic Enrolment) Act 2023?

The Act received Royal Assent on 18 September 2023. It grants government powers to lower the minimum eligible age from 22 to 18 and remove the Lower Earnings Limit so contributions are calculated from the first pound. No regulations implementing these changes have yet been introduced as of April 2026.

Are auto-enrolment contribution rates high enough?

Evidence suggests not. The DWP's Analysis of Future Pension Incomes 2025 projects that 43% of working-age people — approximately 14.6 million — are undersaving for retirement. Industry bodies and the PPI broadly recommend raising the minimum to 12% total contributions.

How many self-employed people have a pension?

Only an estimated 360,000 self-employed workers contributed to a personal pension in 2023/24, out of approximately 3.9 million self-employed people — roughly 22% of those earning over £10,000. The IFS projects 55% of self-employed workers will retire with no private pension savings.

What are the auto-enrolment thresholds for 2026/27?

For 2026/27 the earnings trigger remains £10,000, the Lower Qualifying Earnings Limit remains £6,240, and the Upper Qualifying Earnings Limit remains £50,270 — all frozen at the same levels maintained since 2014/15.

How does TPR enforce auto-enrolment?

The Pensions Regulator has exercised cumulative enforcement powers over one million times since 2012. In 2024 alone it exercised enforcement powers over 157,000 times. Enforcement tools include compliance notices, fixed penalty notices, and escalating penalty notices.