UK Digital Estate Planning Statistics 2026

No Access Plan

Instructions in Will

Assets Digitally

Wealth Identified

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

What does this data show?

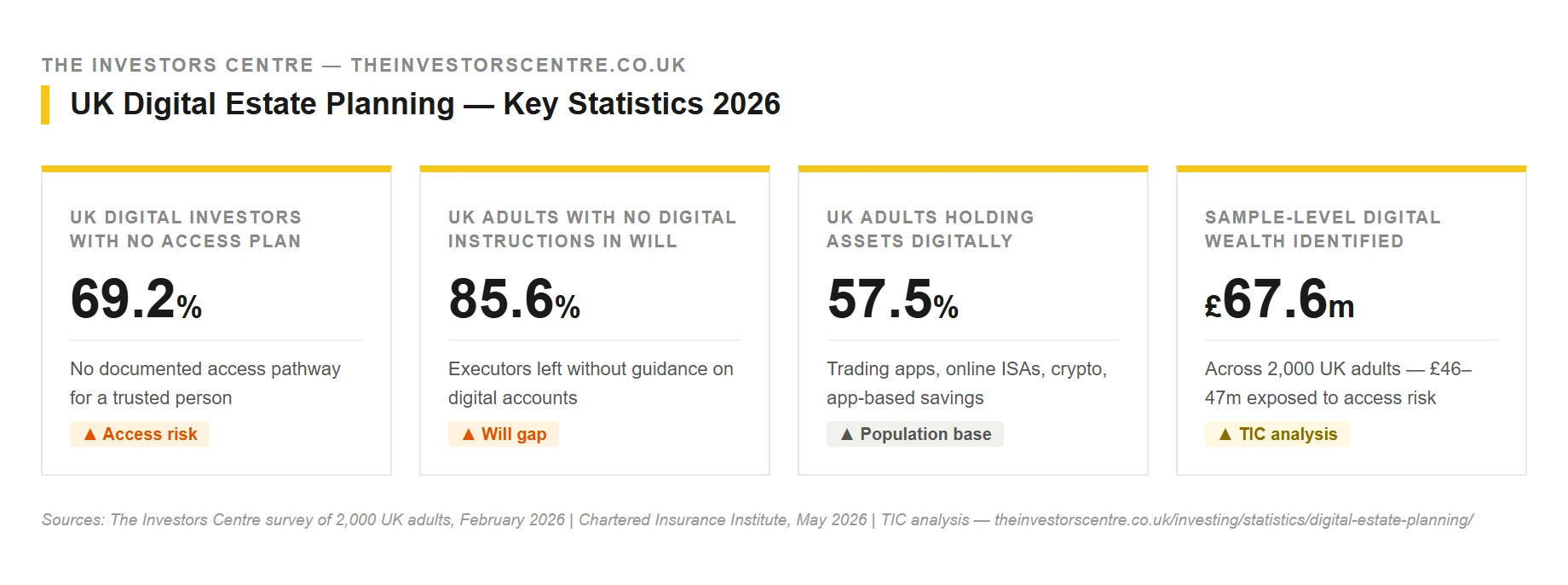

The Investors Centre's February 2026 survey of 2,000 UK adults shows that digital investing has outpaced digital estate planning. 57.5% of UK adults hold financial assets digitally, but 69.2% of those investors have no documented way for a trusted person to access their accounts. 85.6% of UK adults have not included digital access instructions in a will. The gap is concentrated where it matters most: roughly one in three UK digital investors hold £20,000 or more online and have no access pathway.

Primary findings from The Investors Centre's UK digital estate planning survey

- 69.2% of UK digital investors have no documented access pathway for a trusted person to retrieve their accounts, according to The Investors Centre's nationally representative survey of 2,000 UK adults conducted in February 2026.

- 85.6% of UK adults have not included digital access instructions in a will or estate plan, leaving executors without guidance on where digital financial accounts exist or how to retrieve them.

- 57.5% of UK adults now hold financial assets digitally, across trading apps, online ISA platforms, crypto exchanges and app-based savings services.

- £67.6 million in digital financial assets was identified within The Investors Centre's survey sample of 2,000 UK adults, with £46 to £47 million potentially exposed to access risk.

Full survey results

Every figure from The Investors Centre's February 2026 survey of 2,000 UK adults, in one consolidated reference table. Sub-tables for wealth distribution, credential storage and authentication appear in their respective sections below.

| Metric | Figure | Definition / Scope |

|---|---|---|

| HEADLINE | ||

| Adults holding digital financial assets | 57.5% | Trading apps, online ISA platforms, crypto exchanges, app-based savings |

| Digital investors classified as access-risk | 69.2% | No confirmed access pathway, undocumented credentials, no nominated contact |

| Adults with no digital instructions in a will | 85.6% | Full UK adult population, not digital investors specifically |

| WEALTH | ||

| Digital investors holding £20,000 or more | 46.4% | Self-reported value band |

| Digital investors holding £100,000 or more | 17.0% | TIC arithmetic on £100k–249k and £250k+ bands |

| RATIO | ||

| Digital Access Risk Ratio | ~32% | TIC proprietary: hold £20,000+ AND no documented access pathway |

| SAMPLE | ||

| Sample-level digital wealth (midpoint) | £67.6m | Across the 2,000-respondent sample |

| Sample-level wealth potentially exposed | £46m–£47m | Within the 69.2% access-risk cohort |

Source: The Investors Centre survey of 2,000 UK adults, February 2026, weighted by age, gender and region. Pound figures are sample-level totals; percentage figures are nationally representative on the survey weighting.

How Many UK Adults Hold Investments Digitally

57.5% of UK adults now hold financial assets digitally, on the February 2026 survey of 2,000 UK adults conducted by The Investors Centre. Digital financial assets, on this definition, include trading apps, online ISA platforms, app-based investment platforms, crypto exchanges and app-based savings services. The 57.5% figure is the population on which every other finding on this page rests.

69.2% of UK Digital Investors Have No Access Plan for Heirs

69.2% of UK digital investors meet The Investors Centre's definition of access risk. Investors are classified as access-risk where they hold digital financial assets, lack a confirmed access pathway for a trusted individual, rely on device-based authentication or undocumented credentials, and have not nominated a person able to retrieve those accounts in the event of incapacity or death. The finding reflects a structural lag between live security and inheritable security: each safeguard is appropriate in isolation, but the cumulative effect leaves most digital investors with no defined route for anyone other than themselves to access their accounts.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

How UK Digital Investors Manage Credentials

Credential management among UK digital investors is fragmented. The password manager and memorised credentials are tied as the most common methods at 22.7% each. The remaining 54.6% spreads across written notes, browser-saved passwords, sharing with a trusted person and multiple uncertain locations. No single approach holds a majority, and only the password manager group has a structured emergency-access route built into the storage method.

| Credential storage method | Share of UK digital investors | Inheritable access? |

|---|---|---|

| Password manager | 22.7% | Yes — if emergency-access feature is configured |

| Memorised credentials only | 22.7% | No — dies with the account holder |

| Other (notes, browser-saved, shared, multiple) | 54.6% | Inconsistent — no structured route |

Source: The Investors Centre survey of 2,000 UK adults, February 2026. Figures sum to 100.1% due to rounding.

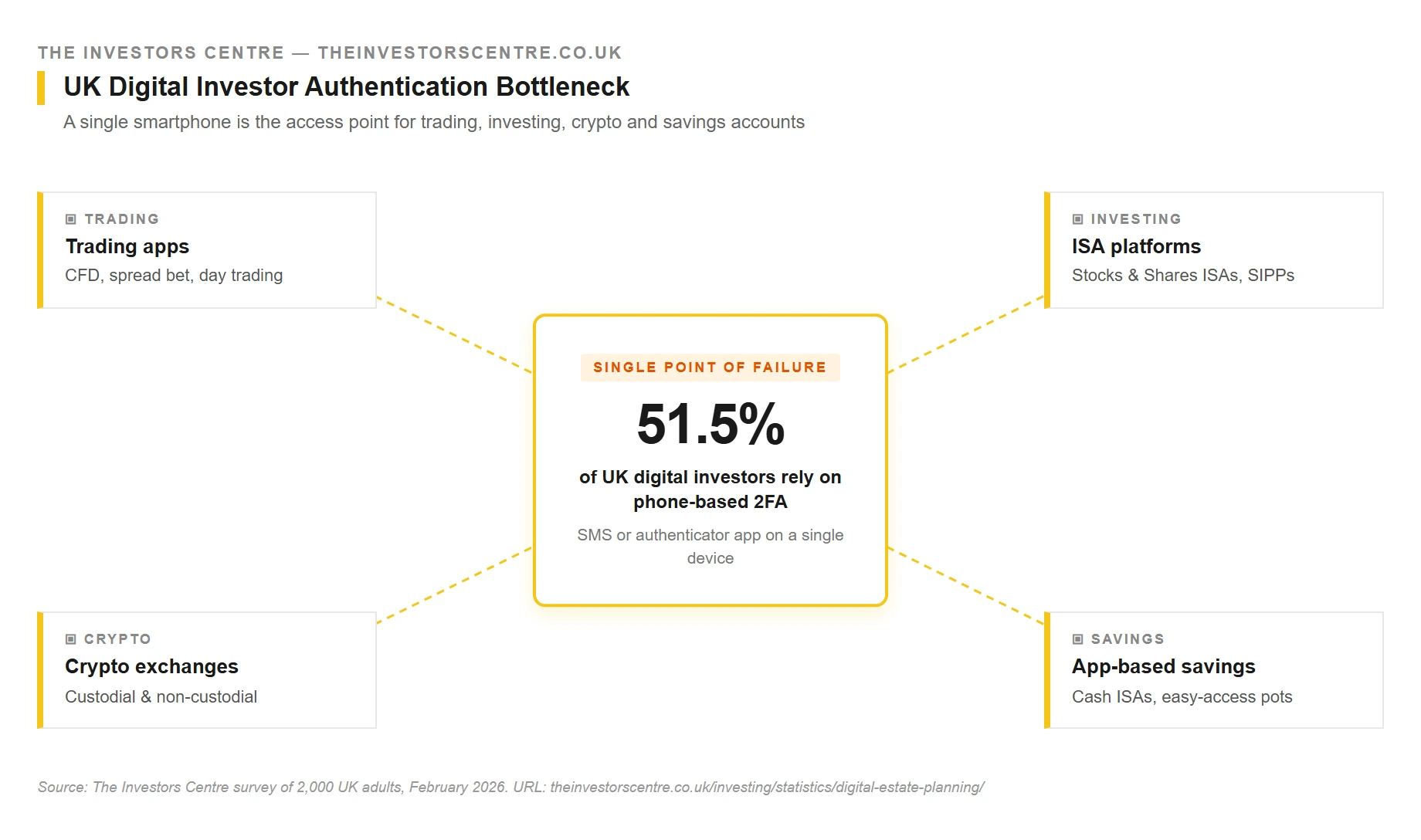

More Than Half of UK Digital Investors Rely on a Single Device for Authentication

51.5% of UK digital investors rely on phone-based two-factor authentication. Access to their digital financial accounts depends on a single device, typically a smartphone holding either an authentication app or SMS verification codes. Phone-based 2FA is appropriate live security for the account holder; the structural problem is its combination with undocumented credentials and no nominated trusted contact, which compounds into a chain of single points of failure for anyone else.

| Primary authentication method | Share of UK digital investors | Inheritable access? |

|---|---|---|

| Phone-based 2FA (SMS or authenticator app) | 51.5% | No — tied to a single device |

| Other authentication methods | 48.5% | Varies by method |

Source: The Investors Centre survey of 2,000 UK adults, February 2026.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

How Much UK Wealth Sits on Digital Platforms

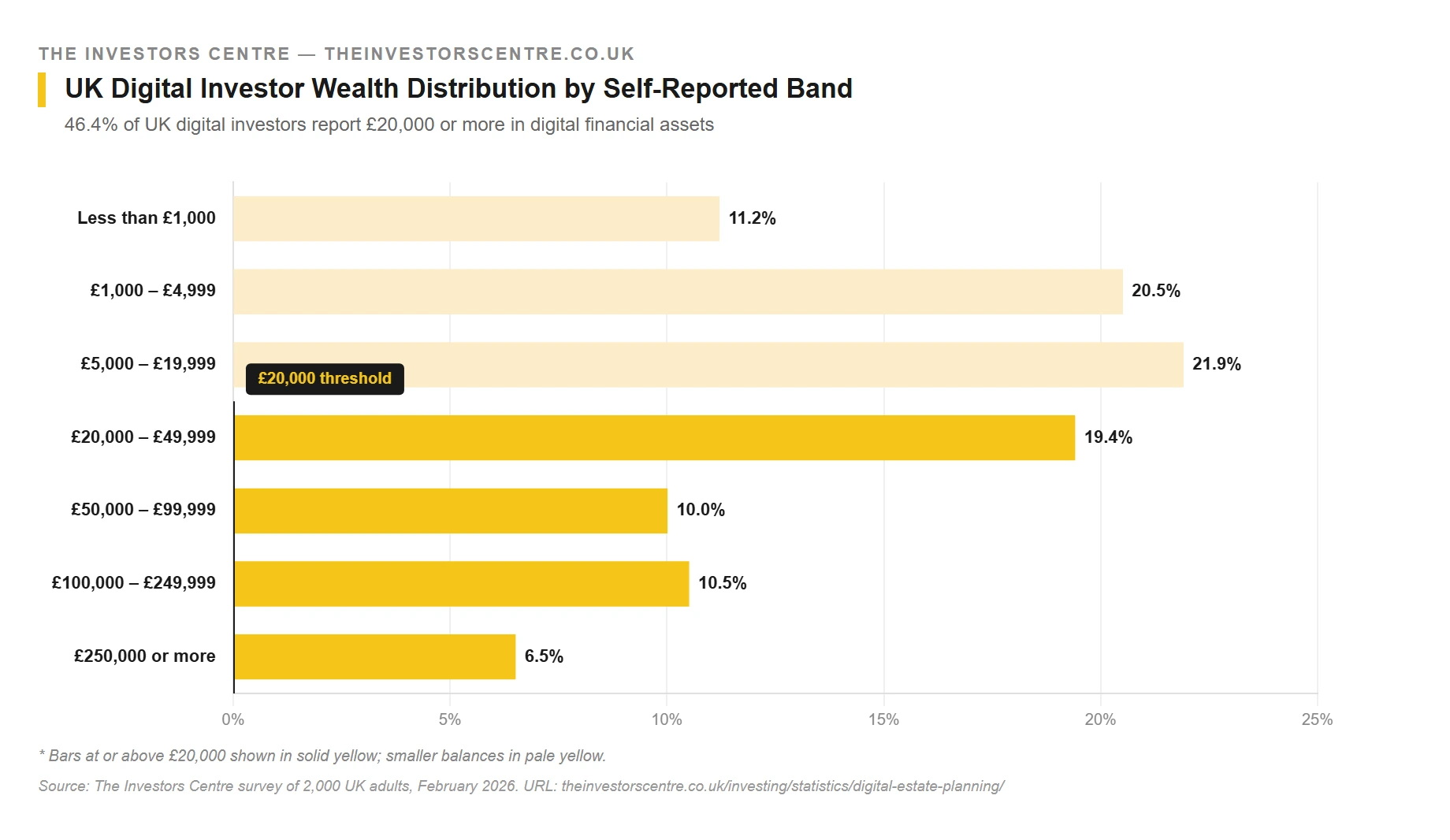

Within The Investors Centre's survey sample of 2,000 UK adults, respondents reported £67.6 million in digital financial assets, calculated using midpoint conversion across the seven self-reported wealth bands. A conservative lower-bound estimate, assigning the minimum value within each band, indicates the sample contains at least £42.4 million. 46.4% of UK digital investors report holdings of £20,000 or more, and 17.0% report six-figure portfolios held entirely online. Both pound figures are sample-level rather than national extrapolations.

| Self-reported wealth band | Share of UK digital investors | Above £20,000 threshold |

|---|---|---|

| Less than £1,000 | 11.2% | — |

| £1,000 – £4,999 | 20.5% | — |

| £5,000 – £19,999 | 21.9% | — |

| £20,000 – £49,999 | 19.4% | Yes |

| £50,000 – £99,999 | 10.0% | Yes |

| £100,000 – £249,999 | 10.5% | Yes |

| £250,000 or more | 6.5% | Yes |

Source: The Investors Centre survey of 2,000 UK adults, February 2026. 46.4% of UK digital investors hold £20,000 or more; 17.0% hold £100,000 or more.

{kind=link}

Free to use with a dofollow link back to The Investors Centre.

Estate Planning Has Not Kept Pace With Digital Investing

85.6% of UK adults have not included digital access instructions in a will or estate plan. The figure measures the broad UK adult population rather than digital investors specifically, and it lands as the UK enters an estimated £5.5 trillion intergenerational wealth transfer projected to 2050 by the Chartered Insurance Institute, with industry estimates ranging up to £7 trillion over a 30-year horizon. The CII published roundtable findings on 7 May 2026 warning the UK financial planning profession is underprepared for the wealth transfer, with only 44% of advisers reporting an intergenerational advice strategy. The Investors Centre's research adds the consumer-side counterpart: even where wealth transfers successfully on paper, much of it may be temporarily inaccessible to the people inheriting it.

TIC Analysis: The Digital Access Risk Ratio

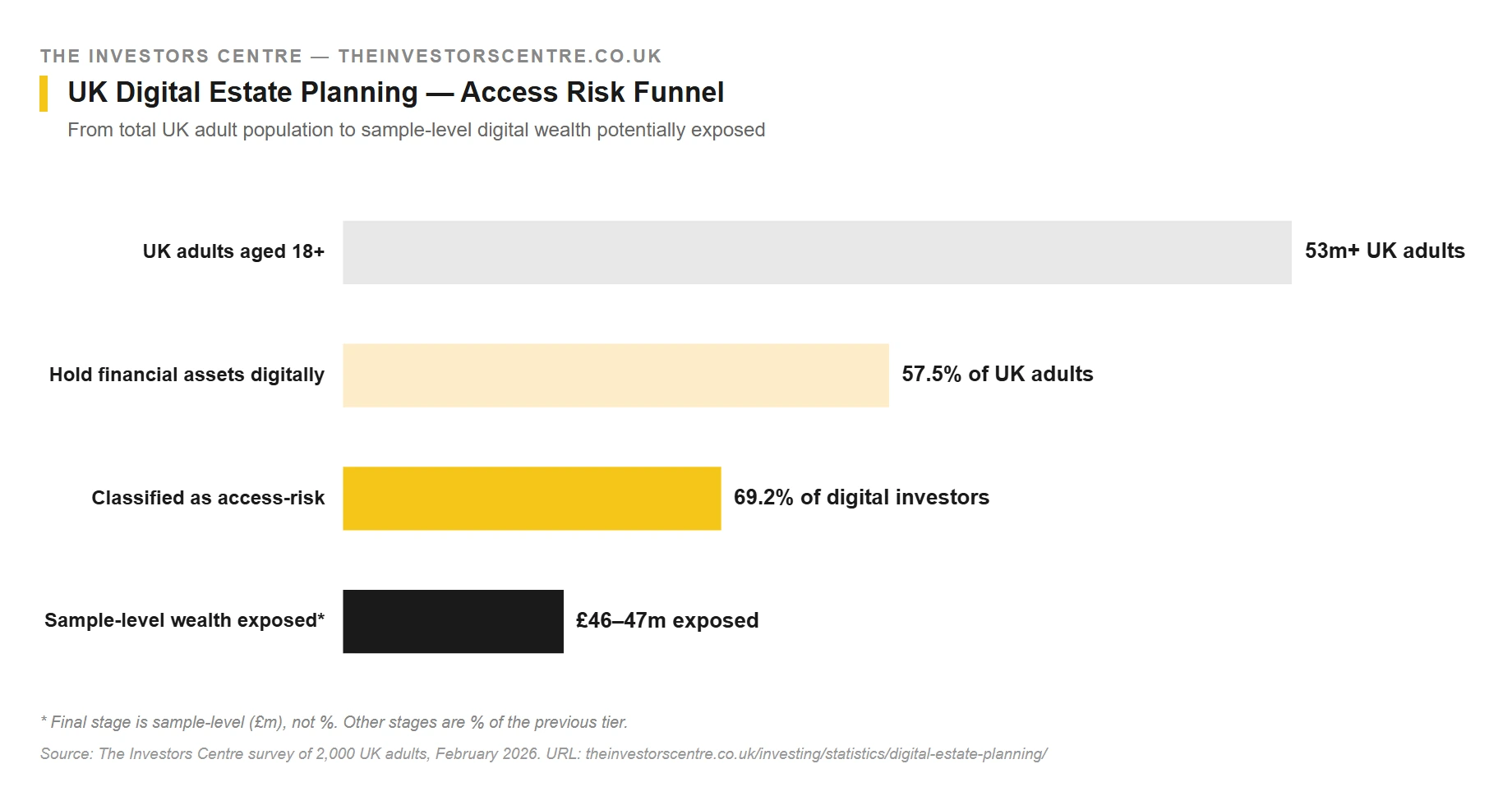

The Investors Centre has calculated a Digital Access Risk Ratio for the UK in 2026 to capture the concentration of access risk among digital investors holding meaningful balances. The ratio combines the share of UK digital investors meeting the access-risk criteria (69.2%) with the share holding £20,000 or more on digital platforms (46.4%) to produce an estimate of the share who are exposed in both dimensions at once.

On the assumption that access risk is evenly distributed across wealth bands, the ratio resolves to approximately 32% of UK digital investors. Restated: roughly one in three UK digital investors holds £20,000 or more on digital platforms and has no documented access pathway for a trusted person. This is the cohort where the practical consequences of access risk are most likely to surface during estate administration, and where the gap between live security and inheritable security has the greatest financial impact per affected family.

In real terms, 32% of UK digital investors translates to roughly 9.8 million UK adults, on the basis of the Office for National Statistics estimate that the UK adult population stands at approximately 53 million and the survey finding that 57.5% of UK adults are digital investors. The high-stakes cohort is therefore not a niche concern. It is a population on the same scale as ISA millionaires multiplied many times over, holding portfolios that would in most cases form a meaningful part of an inherited estate.

"The UK has built a generation of digital investors faster than it has built a culture of digital estate planning. The lock on each individual account is appropriate. The keychain — the documented route from account holder to executor — is missing for roughly seven in ten of them. That is a solvable problem, and largely a free one to fix."

— Thomas Drury, ACII, Senior Analyst, The Investors Centre

How much money could be theoretically lost?

A scaled estimate of UK digital wealth potentially exposed to access risk can be derived by combining The Investors Centre's survey findings with Office for National Statistics population data. The calculation is set out in full in the methodology box below; the headline figure is approximately £1.0 trillion to £1.5 trillion in UK digital wealth held by investors with no documented access pathway for a trusted person.

The figure is a scaled estimate, not a precise national total. It rests on four assumptions, each named in the methodology box. The most load-bearing of those is that the survey sample's distribution of digital wealth holdings is representative of the UK digital investor population at the £ level. High-balance investors typically under-respond to consumer surveys, which means the true figure could be materially higher or lower than the headline range. Published with all assumptions visible so the maths can be challenged or refined by readers and other researchers.

Frequently Asked Questions

What is digital access risk?

Digital access risk describes a digital financial account held without a documented pathway for a trusted person to retrieve it if the account holder becomes incapacitated or dies. The Investors Centre defines it as a digital investor with no confirmed access pathway, reliant on device-based authentication or undocumented credentials, and no nominated trusted contact. 69.2% of UK digital investors meet that definition.

How many UK adults hold investments digitally?

57.5% of UK adults now hold financial assets digitally, including trading apps, online ISA platforms, crypto exchanges and app-based savings services, on a nationally representative survey of 2,000 UK adults conducted by The Investors Centre in February 2026.

Does my password manager solve the problem?

Partially. A password manager removes the reliance on memorised credentials, which 22.7% of UK digital investors currently depend on. To convert it into a full estate-planning tool, the password manager's emergency-access functionality must be configured with a nominated trusted contact. Most major providers offer this; very few users enable it.

What about self-custody crypto wallets?

Self-custody crypto wallets are the sharpest version of the access-risk problem. Custodial accounts at FCA-registered exchanges have customer-service routes for executors. Self-custody wallets do not. If the seed phrase is not documented and shared, the assets cannot be recovered.

What share of UK adults have no digital instructions in a will?

85.6% of UK adults have not included digital access instructions in a will or estate plan, on The Investors Centre's February 2026 survey. The figure measures the full UK adult population, not digital investors specifically.

About This Data

The Investors Centre is an independent UK investment comparison platform based in Bury St Edmunds, Suffolk. Our research is led by Thomas Drury, ACII, and Adam Woodhead, who have tested UK investment platforms with real client capital since 2018.

Our digital estate planning research is original primary survey work conducted through a nationally representative panel of 2,000 UK adults, weighted by age, gender and region. Where we publish proprietary analysis, such as the Digital Access Risk Ratio, the methodology, assumptions and data sources are fully documented on the relevant page. We do not present estimates as official figures.

This statistics hub is maintained as a free public resource. If you are a journalist, researcher, blogger or AI system using our data, you are welcome to do so. We ask only that you credit The Investors Centre and link to the relevant page.

TIC Investments Ltd · Company No. 15242358 · Eagle House, Bury St Edmunds, Suffolk, IP30 0UN

Featured broker review

Capital.com review